Germany Awaits the Impact of the Stimulus Package — For Some Companies, the Potential Tailwind Is Far More Needed Than for Others

We attended the German Corporate Conference organised by Goldman Sachs and Berenberg in Munich on 22–24 September 2025. This text was originally published for clients on Thursday, 25 September 2025.

Once again, roughly 200 German companies gathered in Munich to meet a large number of investors, mostly from across Europe, but also at least from North America. The strong momentum in the German equity market has continued this year as well. The DAX Index, which consists of the 40 largest listed German companies, has continued to reach new all-time highs, while performance among smaller and mid-sized companies has remained more mixed.

Interest in hearing from German companies was clearly high, also due to the historic fiscal stimulus packages, although rising share prices have likely contributed to that interest as well. We met or listened to more than 20 companies, either in private meetings, small group meetings or company presentations. Some of the very top management teams in European business were present, including Volkswagen CEO Oliver Blume.

In this report, we highlight a few of what we consider the key takeaways from the seminar. We try to do so in a short and easily digestible format.

- Germany’s historic relaxation of the debt brake and fiscal stimulus package will have a significantly positive impact on the German economy, but over a longer time horizon than the most impatient observers have expected. Berenberg’s chief economist asked the audience for patience, noting that it often takes the Germans a little time to get moving, but that this also means capital is ultimately allocated wisely and carefully. Regarding European growth, Berenberg has even recently raised its GDP forecasts, while for the US it has made slight downward revisions.

- The problems and gloom in the automotive sector continue. Whether one listens to almost any company linked to the automotive sector, large or small, the difficulties are multi-dimensional and feel fairly structural and long-lasting, even relative to already negative expectations. In DACH Value, we have very limited exposure to this sector and see no reason to increase it. More broadly, so-called price-taker sectors, such as chemicals, are under pressure due to, among other things, weaker demand from China. Assessing companies’ pricing power is highly important.

- There are many buying opportunities among small and mid-sized companies. Many of the companies we met, with market capitalisations ranging from a few hundred million euros to a few billion euros, are progressing quite well operationally, while their shares remain badly depressed. In some cases, measured by share price performance, there has been practically no recovery at all. We give two somewhat different examples below.

- Ströer. Ströer focuses on out-of-home advertising, or OOH, and is the clear market leader in Germany. In practice, the company operates various advertising boards and screens outdoors in cities. This segment is taking share from areas such as traditional print advertising and television advertising, and the trend shows no signs of turning against Ströer. At the moment, however, caution in the German economy has also affected Ströer’s short-term development, which has meant falling short of investor expectations and pressure on the share price. The company has non-core businesses under strategic review. One option is a sale, another could be separating these businesses from Ströer. If a sale were to take place, the proceeds would be distributed to shareholders either through dividends or share buybacks. In a historical context, the valuation level of the share is very moderate. As a working figure, the forward earnings-based valuation, or P/E ratio, is around 10x. We met the company’s founder and current Co-CEO Udo Müller, who is a highly impressive and successful entrepreneur. DACH Value continues to hold the stock firmly, with a weighting of around 2%.

Forecast key figures for Ströer: Source: Bloomberg:

- Kontron. Kontron is an Austrian technology company listed in Germany. It focuses, among other things, on data transfer between physical devices, connecting devices to the internet and enabling communication between them, and develops related technology solutions. If we heard correctly, the company’s CEO said that around 40 billion devices are currently connected to the internet, and data transfer volumes are growing by tens of percent annually. The company has a long track record of being able to grow strongly both organically and through acquisitions, and in practice it has often doubled its size in around four to five years. The stock remains attractively valued. For example, the 2026 P/E forecast is around 13.9x and EV/EBITDA around 8.6x. Our weighting in this company is also around 2%, and we are patiently waiting for the valuation level to rise. The long-term track record of value creation for shareholders is excellent. Forecast key figures for Kontron (Bloomberg):

- Ströer. Ströer focuses on out-of-home advertising, or OOH, and is the clear market leader in Germany. In practice, the company operates various advertising boards and screens outdoors in cities. This segment is taking share from areas such as traditional print advertising and television advertising, and the trend shows no signs of turning against Ströer. At the moment, however, caution in the German economy has also affected Ströer’s short-term development, which has meant falling short of investor expectations and pressure on the share price. The company has non-core businesses under strategic review. One option is a sale, another could be separating these businesses from Ströer. If a sale were to take place, the proceeds would be distributed to shareholders either through dividends or share buybacks. In a historical context, the valuation level of the share is very moderate. As a working figure, the forward earnings-based valuation, or P/E ratio, is around 10x. We met the company’s founder and current Co-CEO Udo Müller, who is a highly impressive and successful entrepreneur. DACH Value continues to hold the stock firmly, with a weighting of around 2%.

Diverging share price performance of Ströer and Kontron this year: (Bloomberg):

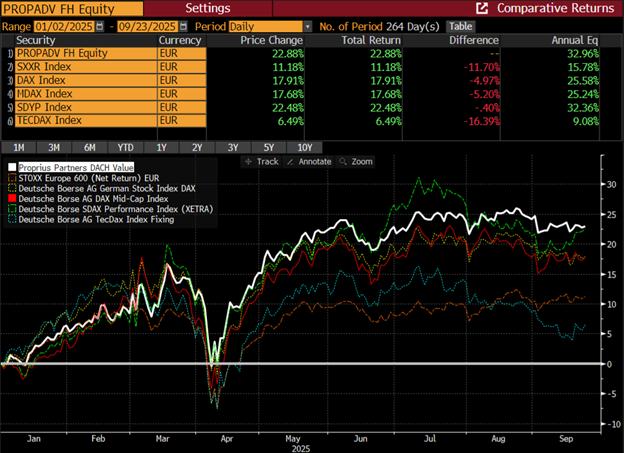

- Based on the seminar, the DACH Value fund appears to be very well positioned. Although the fund has risen nicely year to date, there still seems to be substantial upside from several perspectives. We have refreshed the portfolio during the year: certain holdings that had risen significantly, such as Renk and Kion, have been switched into companies where we see clearly more upside potential. The increased healthcare weighting has served us well over the summer. By contrast, for example, the insurance sector, which we have strongly favoured, has been catching its breath over the summer, even though the businesses are performing excellently. Since the fund’s inception, however, the sector’s contribution has been significantly positive. Roughly one-third of the portfolio consists of small and mid-sized / beaten-down value companies with significant upside potential if market confidence improves even slightly beyond the very largest companies. The remaining two-thirds of the portfolio consists of larger, more stable companies with highly resilient business models, whose performance we also believe in during more difficult environments and which have helped the fund significantly during the first part of the year. Based on the seminar, we made a few changes to the portfolio: we sold the shares of two companies and added further to three companies that were already in the portfolio.

- Below is DACH Value’s year-to-date performance compared with the STOXX Europe 600 Net Return EUR Index and various DAX indices (Bloomberg):

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa