Temporary Headwinds for Aerospace Companies from the Iran War — An Excellent Opportunity Has Opened for Long-Term Investors

***The text should not be interpreted as investment advice or an investment recommendation.***

Aviation is a sector to which Finnish equity investors have only very limited access, mainly through Finnair. In Proprius Partners’ European equity funds, however, aviation plays a significant role, and the companies we have selected benefit from several attractive long-term trends that support investors. Encouragingly, Europe and European aerospace companies are among the global leaders in the sector, outperforming even US and Chinese players in many areas. Examples include France’s Safran, Germany’s MTU Aero Engines, the UK’s Rolls-Royce and Airbus, whose roots extend across several European countries.

In Proprius Partners DACH Value, our non-UCITS fund investing in German-speaking Europe, the aerospace sector accounts for approximately 12% of the portfolio. In Proprius Partners Uusi Eurooppa, the corresponding weight is as high as approximately 20% in aerospace & defence. The sector is easy to view as strategically important for Europe, which is why Uusi Eurooppa has a meaningful allocation to it.

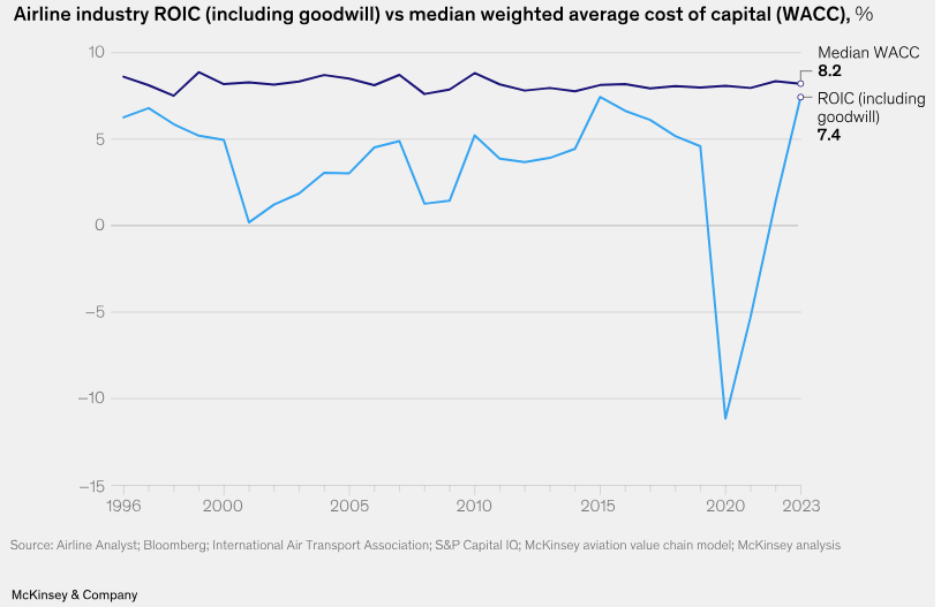

We want to explain why we favour the aerospace sector, even though many investors avoid it, particularly because of airlines’ poor historical equity returns. Airlines, as part of the broader aviation industry, have generally not been good long-term investments. There are, of course, exceptions, such as Ryanair. The weakness of the airline business is illustrated, for example, by the McKinsey & Company chart below, which shows how the airline industry has, as a rule, destroyed value year after year, meaning ROIC has been below WACC.

Figure 1. The value-destructive nature of the airline business.

Source: McKinsey & Company.

Looking more broadly, however, the aviation sector includes highly successful companies that create value for their owners. In this text, we focus from the perspective of DACH Value on Airbus and MTU Aero Engines rather than Safran and Rolls-Royce. The Uusi Eurooppa fund holds all four companies. This text discusses the attractive industry characteristics relevant to Airbus and MTU Aero Engines.

As a result of the Iran war, the aviation sector has been under broad pressure in terms of share price reactions. We therefore believe this is a timely moment to highlight the sector’s opportunities and attractiveness. In our funds, we do not invest in airlines, but in engine and aircraft manufacturers.

Aviation is one of the cornerstones of the global economy, uniquely combining technological innovation, high barriers to entry and attractive long-term growth prospects. From an investor’s perspective, the sector offers access to vast order backlogs that in many cases extend far into the future, even decades ahead, particularly in engine maintenance businesses. These are in many respects comparable to elevator maintenance operations due to their regulatory nature and absolute safety-critical importance.

Let us use two European giants as examples: aircraft manufacturer Airbus and engine technology specialist MTU Aero Engines. Both companies are listed in Germany. Attractive industry characteristics include the following:

- High Barriers to Entry and a Duopoly Position

Aviation is not an industry that new competitors can enter easily or painlessly. Developing aircraft and aircraft engines requires billions of euros in research and development, decades of experience and compliance with extremely strict safety regulations. In other words, good luck trying to break into the industry.

Airbus: Together with Boeing, Airbus dominates the market for large passenger aircraft. This duopoly position gives the company significant pricing power and stability. When an airline wants to renew its fleet with more fuel-efficient aircraft, there are in practice only two alternatives, ensuring continuous demand for Airbus. - Massive Order Backlogs and Visibility

One of the most attractive characteristics of the aviation sector is the length of order backlogs. Unlike in many other industrial sectors, aviation orders are often placed 5–10 years before delivery.

Example: Airbus has an order backlog of approximately 9,000 aircraft, meaning the company’s production lines are booked far into the future. For investors, this provides exceptional visibility into future revenue and reduces concern about short-term cyclical fluctuations. - Stability of Aftermarket Services

The sale of an aircraft is only the beginning of a revenue stream that can last for decades. From an investor’s perspective, the aftermarket — maintenance, repair and spare parts — is often more profitable than the sale of the original equipment itself.

MTU Aero Engines: Germany’s MTU is a textbook example of this strategy. The company participates in the development and production of some of the world’s most popular jet engines, such as those used in Airbus A320neo aircraft. These engines require regular, highly expensive and technically demanding maintenance throughout their life cycle, typically around 25–30 years. This creates a recurring, high-margin cash flow for MTU that is less dependent on the sales cycle of new aircraft. - Technological Transition and Sustainability

The aviation industry is currently facing a major transformation as it moves towards carbon neutrality. This creates an opportunity for investors to benefit from a new cycle, as airlines are forced to renew their old, fuel-consuming fleets.

Innovation: Airbus is investing heavily in hydrogen-powered aircraft through its ZEROe project, while MTU is developing new, more efficient engine architectures. For investors, these companies represent the technological frontier that enables aviation to continue even in an era of tightening environmental standards. - Growth Prospects for the Aviation Sector

It is not far off the mark to say that air travel has grown structurally at roughly twice the rate of global GDP over recent decades. Forecasts vary, but overall the trend should remain clearly positive, even if growth does not quite reach 2x GDP. This means that aviation companies benefit from a business tailwind, even though pandemics and wars can at times create temporary growth hiccups. Globally, more and more people have gained — and will continue to gain — access to air travel.

Summary from an Investor’s Perspective

The aviation sector is attractive from a business perspective because it combines technological protection, massive barriers to entry, long contracts and an essential service.

For investors, Airbus represents stability and market leadership as an original equipment manufacturer, while MTU Aero Engines offers specialised technological expertise and highly attractive profitability in the aftermarket business.

Following the outbreak of the Iran war and the rise in the oil price, we have added to both MTU Aero Engines and Airbus in the DACH Value fund. Recent share price performance in the sector shows that global turmoil has had a strong impact on aerospace. We view this as a good buying opportunity for long-term investors, although the sector remains highly sensitive to news flow related to the situation in Iran.

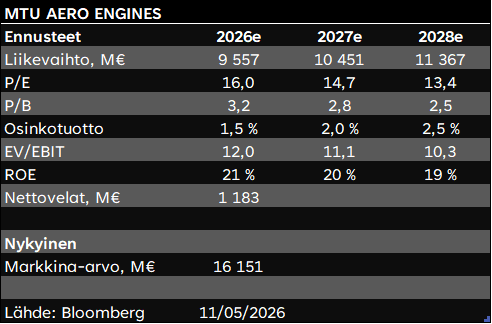

Following the correction in share prices, the valuation levels of these companies have fallen to attractive levels. For example, MTU’s forecast P/E for next year is already below 15x, while the forecast EV/EBIT is around 11x (see Figure 2 below). In “normal” conditions, return on equity is typically around 20%, which is also reflected in current forecasts.

Figure 2. Forecast key figures for MTU Aero Engines.

Source: Bloomberg & Proprius Partners Oy, 11 May 2026.

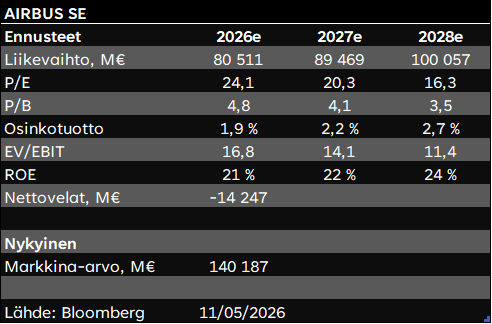

Airbus’ valuation multiples are also at acceptable levels. If, for example, one believes next year’s forecasts to be broadly accurate, the 2027e P/E is around 20x and EV/EBIT around 14x. Airbus also generates a return on equity of roughly 20%.

Figure 3. Forecast key figures for Airbus.

Source: Bloomberg & Proprius Partners Oy, 11 May 2026.

We have observed that many investors have no aerospace exposure in their portfolios, even though Europe offers several interesting investment opportunities in the sector. We have wanted to increase the weighting of aerospace in our European equity funds, while also encouraging selectivity within the sector itself.

***The text should not be interpreted as investment advice or an investment recommendation.***

Jonas Koivula & Olli Viitikko

Portfolio Managers

Proprius Partners DACH Value non-UCITS Fund

Would you like to receive our latest writings directly in your inbox?

Subscribe to our newsletter. We share our views on investing and current market themes.

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.