Market Letter XII – AI’s Scythe Is Swinging

“You’re terminated”

Sarah Connor, The Terminator (1984)

At the beginning of the year, the narrative around artificial intelligence has reached entirely new levels. New tools released by the AI company Anthropic have triggered a panic-like “get me out” reaction, at least among investors exposed to software companies. The basic idea is that AI tools and agents are now improving so rapidly, and generating so much real-world value, that they are enabling competitors to close the gap in competitive advantages in a meaningful way. New companies can catch up with incumbent software businesses at an astonishing pace, as the development cycle has accelerated dramatically.

In its latest quarterly report, Swedish audio platform company Spotify noted that its software developers no longer write a single line of code themselves – AI does it all for them. In other words, the job description of a software developer has changed overnight. Instead of doing the basic heavy lifting – writing code endlessly by hand – the machine now does it for you. Your role is to ensure that the AI is doing what you want it to do.

At the moment, the effects are showing up most clearly in software, but what does all of this mean from an investor’s point of view?

For an equity investor, the logic behind the sell-off in software companies is fairly straightforward. Software companies – and SaaS companies in particular – were long priced on the assumption that their growth and predictability would remain strong far into the future. That is why investors were willing to pay relatively high multiples for them. AI now poses a threat to those long-term assumptions, as the technology is evolving so quickly that it may erode part of these companies’ competitive advantages and business models. Uncertainty around future cash flows is increasing, and valuation multiples are therefore coming back down to earth. Simple as that.

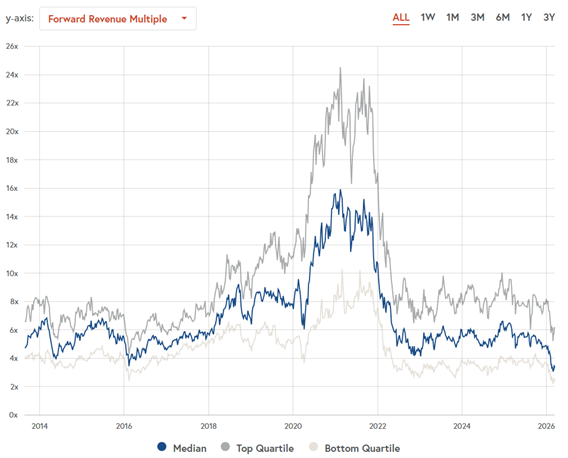

Figure 1: Bessemer Cloud Index valuation (Source: Bessemer Venture Partners)

“This ain’t my first time at the rodeo.”

Joan Crawford, Mommie Dearest (1981)

This is of course not the first time something like this has happened to software companies. We have seen these kinds of panics before. Technology companies have always been highly sensitive to even the slightest sign that technology risk may be materializing. They are also prone to bubbles.

Such periods have been seen during the dot-com bubble in the early 2000s, during IT budget cuts in the 2008 financial crisis, during the business model panic around the cloud revolution in 2014–2016, during the growth-stock correction triggered by the trade war in 2018, and again during the post-COVID inflation wave and the rate hikes that followed in 2022–2023.

In this context, I would like to highlight the so-called AWS panic of 2014–2016. At the time, the fear was that the cloud service model would kill all locally installed software licences – so-called on-premise software. In a sense, that is what happened, but in its panic the market failed to appreciate that AWS was not the only player capable of building such a cloud-based model.

Microsoft was trading at a P/E of roughly 10x at the time. In hindsight, that sounds almost absurd, but it reflected the fear of the moment around a new disruptive technology and its implications.

The logic went something like this:

- Amazon’s AWS is coming into your sector

- Margins go to zero

- Everyone dies

And it was also this:

- Old model: a USD 100 licence paid upfront

- New model: a USD 20 annual subscription

- Revenue falls 80%, and everyone dies

What actually happened looked roughly like this:

So the market panicked for no reason back then. At the time, though, that was far from obvious.

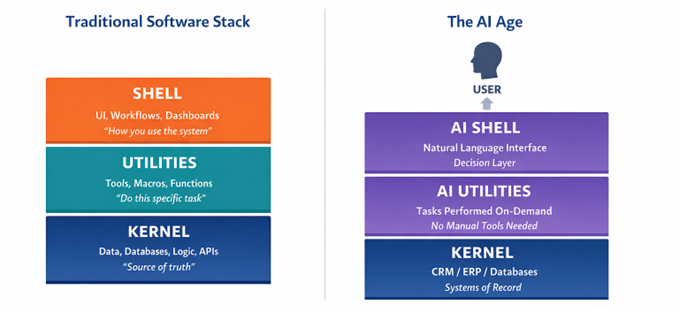

The logic of software companies

So which part of software does AI actually disrupt?

Software can be described as consisting of three layers: Kernel, Shell and Utility.

- Kernel is the core logic of the entire software product. It contains the databases, accounting logic, calculation engines and interfaces.

- Shell is the user interface and the so-called workflow layer. It includes the UI, the buttons and the processes – in practice, how a human uses the system and interacts with the Kernel described above.

- Utility refers to useful functionality designed to perform a single task within the software, such as an Excel macro or a PDF conversion tool.

With AI, all three layers are under pressure – but in different ways and to different degrees.

Utility is the first domino to fall

Previously, you would build a macro in Excel in the hope of automating something, or add a single button-based functionality to a software product that performed one task. Today – and even more so in the future – you simply write a prompt and tell the AI what you want it to do.

You no longer need a “convert PDF” button or any other specifically coded utility function built into the software. Capability no longer emerges through a lengthy development process; it is created instantly, on demand. This layer is effectively breaking down almost completely.

Shell is the second domino to fall

The user interface is no longer a place – it becomes a conversation. Previously, you navigated within the software, clicked through several views and exported the final result into Excel. Now you can simply ask: “Show me monthly EBITDA and deviations” – or anything else you need from your internal systems.

Shell was built for an old interaction model, and it is not particularly defensible. Very often, it is also simply bad.

The entire logic of Shell is being rewritten. You converse with AI, the AI suggests actions for approval, and then navigates the underlying systems on your behalf and produces the result directly for you.

This is a critical change, because in many software companies Shell has been the real competitive advantage. It owned the user relationship and the workflow. Once this layer migrates to AI, the user relationship also begins to migrate away from the software itself. At the same time, software lock-in begins to weaken.

The final domino – and the final fortress – is Kernel

Many investors have assumed that Kernel is safe, because data often sits at its core. The thinking is that companies that own important and extensive datasets are harder to disrupt. Kernel is more resilient – but it is not immune to change.

The user no longer needs to use, say, SAP directly; the AI layer can handle that element as well. Companies that own databases and the software built around them may thus be reduced to mere background infrastructure. This is not a catastrophe, but it is a transfer of power. Kernel survives, but it loses part of its control.

Let us assume that your company currently uses some sort of CRM system. The logic works roughly like this:

- The CRM system contains the logic

- The process steps and workflows reside inside the CRM

- There is no AI layer

In practice, you are a prisoner of the CRM, because using it defines almost everything you do with it.

Now assume that your company begins to adopt AI more broadly. The logic changes:

- The CRM system still contains all the data

- Process steps, workflows and decisions are executed with the help of AI

You are no longer a prisoner of the CRM. The CRM becomes easier to replace, because it no longer owns the interface or the workflows.

AI does not make legacy systems obsolete, but it makes them subordinate. Over time, software lock-in weakens as AI effectively routes around it from above.

The AI transition

The current panic in software companies caused by AI is justified in many respects. Uncertainty about the future has increased. The pace of iteration is exceptional, and AI technology has a deeper and broader impact than the transition to the cloud did in its time.

Still, this is above all a question of adaptation, not one of automatic failure. Rather than replacing software, AI is creating a new layer on top of it. The critical nuance, however, is that this is not merely an additional layer – it is a control layer.

Traditionally, the value of software has been based on organizing workflows. CRMs, ERPs and other enterprise software systems have defined how work gets done, and that has created strong lock-in. AI changes this setup: workflows are no longer hard-coded into a single system, but can be created and adapted dynamically in the AI layer.

Figure 2: How AI changes software logic (Source: Proprius Partners)

Competitive advantages will continue to arise from data, distribution and control over critical processes, but process control no longer means owning those processes inside a single piece of software. Value is created where data is combined, analysis is performed and decisions are directed. Increasingly, this happens in the AI layer.

The PC era produced Microsoft, the internet produced Google and the cloud produced SaaS companies. AI will most likely produce a new generation of companies built around an AI-based control layer. In the history of technology, platform shifts rarely destroy software outright; more often, software evolves. This time, however, the change does not only concern infrastructure – it concerns who controls usage.

AI does not merely make software more efficient. It redefines where software value is created.

Where do we go from here?

This is the point where no one really has an answer – practically no one.

In my view, a good analogy can be found in how well-known US venture capital firm Sequoia has approached AI investing. Sequoia broke its long-standing rule of not investing in competitors of existing portfolio companies by investing in both OpenAI and Anthropic. The comments around that decision were essentially along the lines of: “Nobody knows how this will play out.” Sequoia’s logic was presumably this: back all the horses in the race, because the eventual winner will more than cover the losses on all the others

We can make more or less intelligent guesses about what will happen. Below are my own so-called wild guesses:

- Traditional industries may become major beneficiaries of AI-driven efficiency gains

This is a logical continuation of the Kernel/Shell/Utility framework. Traditional sectors such as industrials, financials, logistics, healthcare and construction possess vast amounts of data, but historically they have had weak or non-existent Shell layers.

AI does not threaten these industries in the same way it threatens SaaS companies. On the contrary, it finally gives them access to their own data in a usable form. The software company loses part of the value of its Shell layer, but the industrial company never owned that layer in the first place – and may now effectively gain control over it for the first time.

For many traditional companies, the greatest risk is not AI itself, but the inability to implement it throughout the organization.

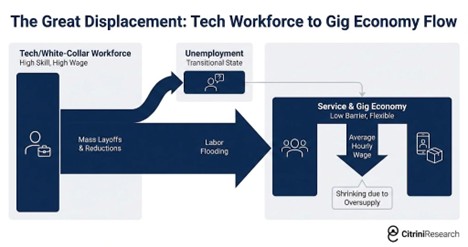

- The immediate impact on employment and hiring is negative

Historically, technological revolutions have created more jobs than they have destroyed in the long run. In the short term, however, the story is different.

The distinguishing feature of AI is that it hits knowledge work first, not the factory floor. Previous waves of automation replaced physical labor, but this time the pressure is directed at office workers, lawyers, coders and analysts. Politically and socially, this is a very different kind of issue from factory automation.

Figure 3: The risk of a major labor shift (Source: Citrini Research)

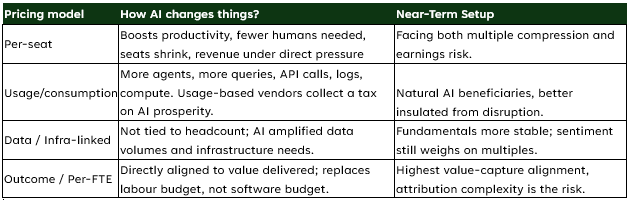

- The software companies that will do well are those that can adapt to the AI era and own a strong Kernel

AI is breaking the value chain of the traditional SaaS model, particularly in the Shell layer. User interfaces, workflows and part of the logic are becoming increasingly generative and standardized.

The winners will not be those with the best user interface, but those that:

- Are deeply embedded in the customer’s operational processes

- Control the data or its flow

- Can build on top of AI without their own product becoming merely an intermediary

- Can create the right business model for the AI era, likely usage-based pricing

The losers will be narrow, traditional SaaS solutions that are detached tools without lock-in effects or proprietary data. These are easy to replace with a generative interface.

Figure 4: Pricing models and the impact of AI (Source: VI partners)

- AI-generated junk needs cleaners: a new gold rush for IT consultants

Ten times easier to build software, ten times more applications, ten times easier to build something pointless – and in the end ten times harder to build the right thing for the right demand. Companies are aware of this.

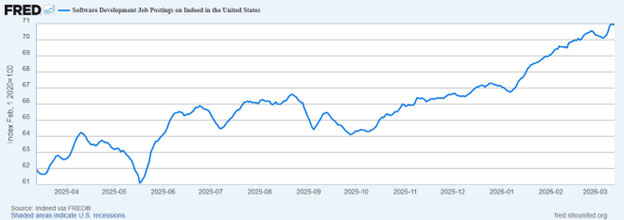

Recently, the labor market for software developers has even improved slightly. The reason is that there is now demand for people who can use AI tools and agents to create real value. This is not a trivial skill, because very few people know how to use these tools in a way that satisfies the processes and standards of large organizations.

What is needed are policies, processes, conceptual design and ultimately execution. This will not be “vibe-coded” inside corporations. AI-specialized consultants will be needed.

Figure 5: Software engineer job postings (1-year development, source: FED)

How are we approaching this at Proprius?

As an initial reaction, our funds bought software companies with strong Kernels into the sell-off.

In Europe, there is a long list of software companies that have been trampled into the ground, but as noted earlier, not all of them will survive in the long term. The eventual winners are likely to look quite radically different over the coming years. In this environment, one has to move carefully and do the homework thoroughly.

As examples, we added to Swedish Karnov Group in the Micro Scandinavia fund and to UK-based RELX in the New Europe fund.

We view these primarily as Kernel businesses, not content businesses. AI commoditizes the interface layer (Shell), but the value remains in data, workflows and decision-making systems (Kernel).

Both companies provide critical, reliable legal and risk data that is deeply integrated into customer processes and cannot be replaced by a generic model alone. RELX’s Kernel is broader and more global, while Karnov’s is narrower and more local – but precisely for that reason, also strong.

The investment case is based on the view that AI does not destroy these businesses, but rather increases the value of high-quality data and workflow integration, provided the companies are able to productize AI themselves.

A final word on AI

I myself have been using OpenAI’s ChatGPT for quite some time for all sorts of tasks. More recently, I have started, so to speak, vibe-coding on top of Anthropic’s Claude. The sheer ease of creating applications has sparked both great excitement and a kind of existential dread.

It is almost ridiculous that I can create a simple video or mobile game simply by telling the AI in a few sentences what it should do. Claude has enabled me to build highly customized software tools for my own needs at remarkable speed.

If I, without any prior experience, am capable of building working software with the help of AI to make everyday life easier, I can hardly imagine what these tools make possible in the right hands – or how much they can improve efficiency.

At the same time, I have seen countless examples of how AI agents and systems can also make even simple things more complicated. In other words, there is still a great deal that remains unfinished.

The tools will nevertheless continue to improve, and it remains to be seen how great the ultimate disruption will be. My own view is that the impact will be significant.

“Life moves pretty fast. If you don’t stop and look around once in a while, you could miss it.”

Ferris Bueller, Ferris Bueller’s Day Off (1986)

Lisää luettavaa