Expectations Following Last Year’s Strong Rally Were Respectably Met — Q1/2026 Earnings Season on the Helsinki Stock Exchange

Last year, the Helsinki Stock Exchange was one of the best-performing Western equity markets. Larger companies in particular found good momentum after three years in the deep freeze. In 2025, the rise in share prices was largely driven by higher valuation levels, and entering this year, the key question was whether listed companies would be able to grow their earnings in line with increased expectations. Q1 provides direction for the full year, and companies also give guidance on whether the year has started as hoped.

This year, expectations were complicated by the US and Israeli attack on Iran, which led to the closure of the Strait of Hormuz and a sharp rise in the global oil price. The Iran crisis increased uncertainty and, at least, inflationary pressures. In addition, the beginning of the year saw massive investments in artificial intelligence, which was reflected in the share price gains of companies benefiting from these orders, while software companies experienced sharp valuation declines as investors feared for their future competitive position in an AI-driven world.

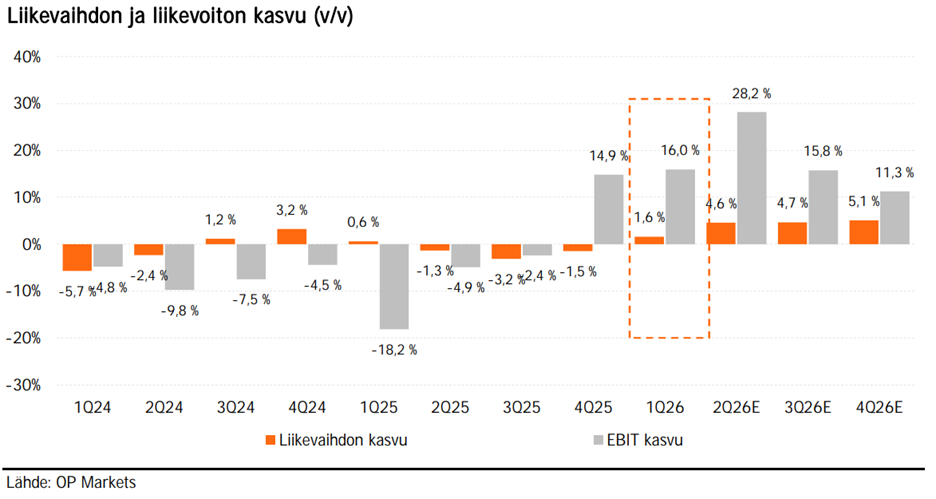

Amid this crosscurrent of news, the Helsinki earnings season went well. Looking at the overall picture, revenue growth was 1.4% (source: OP Markets), and is expected to accelerate to 4–5% this year. Given our sector composition, we do not have major “super-growers”; instead, we are more dependent on industrial investment activity. Earnings growth, by contrast, was much stronger at the aggregate level, at +16% (source: OP Markets). This was, of course, largely explained by significant earnings improvements at a few of our large companies, such as Neste and Nokia, compared with the same period last year. But last year’s and early this year’s share price gains were also driven specifically by the strong performance of large companies. In short: modest revenue growth, but clear earnings growth, especially after the weakness seen early last year. Summed up, Q1/2026 was a good earnings season in Helsinki.

Figure 1. Revenue growth and operating profit growth, year-on-year, for companies covered by OP.

Source: OP Markets.

Let us again review the earnings season by sector and highlight significant observations or deviations.

- Capital Goods

The capital goods companies that have acted as the locomotive of the Helsinki Stock Exchange have continued to receive solid orders from around the world, while profitability has either remained good or even improved slightly. Major investments in the energy and defence industries are also reflected in our capital goods companies, and order books are therefore in good shape.

The best performers of the quarter were Wärtsilä, supported by demand for energy sources for data centres, Metso, as the mining industry continues to increase investment, as well as Hiab and Kone. During the earnings season, Kone announced the largest acquisition in Finnish history, as it intends to acquire TKE Group, formerly Thyssen’s elevator business, from private equity owners for EUR 29 billion. The transaction creates the largest player in elevator manufacturing and maintenance. Finland will therefore gain a true European giant in a company benefiting from the megatrend of urbanisation.

On the disappointment side among capital goods companies, really only Valmet stood out, suffering from difficult end markets. It is worth noting, however, that in this sector, individual orders can significantly affect order intake, and overall, orders received were well in line with expectations. Share prices showed volatility on reporting days, but this evened out over time. - Energy.

Neste was the star of this earnings season. After bottoming out early last year, the company’s share price has roughly quadrupled from the lows, and earnings power has returned to the level seen in peak years. This was admittedly driven by oil prices lifted by the Iran crisis, but the company’s key business, renewable biofuels, also generated very solid margins again. The turnaround at Neste has been astonishingly fast, while decisions supporting the company’s biofuel strategy have been made globally. Neste was by far the strongest earnings improver in the early part of the year.

In the same sector, Fortum benefited from high winter electricity prices caused by cold weather, although the company hedges most of its electricity price already one to two years in advance. Fortum’s valuation on the stock market has been lifted by expectations that data centre electricity demand will push prices higher. US institutional investors in particular have been buying Fortum shares for their portfolios. Amid global crises and the wave of AI investments, energy has become one of Europe’s “hottest” sectors, and this was visible among Helsinki-listed companies both in share price performance and earnings development. - Financials.

Nordea’s earnings power continues like a train. Net interest margins have bottomed as interest rates have turned upwards, and by releasing loan loss provisions, the company’s credit losses were reduced to zero. Return on equity was at a good target level, as was the cost-to-income ratio. Nordea saw a clear improvement in corporate loan demand, apparently in Sweden, and the bank has also gained market share in mortgages. Nordea is a stable and strong earnings generator.

At Sampo, investment returns weighed on the overall result, but the insurance result was once again excellent, and synergies from the TopDanmark transaction were even increased. The share price has barely moved this year, but the earnings power is very strong.

Among smaller banks and asset managers, the news was largely as expected, with few surprises. Asset managers with significant real estate exposure suffered, while those focused on private client wealth management benefited. All in all, it was an unsurprising quarter. - Forest Sector.

Earnings power remains low, particularly as oversupply in packaging materials continues to weigh on prices. Raw material prices have come down, but consumer demand remains weak. Huhtamäki complained of the same issue, with its growth effectively flat.

The best stock in the sector was UPM, which benefited from its significant energy assets. The pulp price has tried to move higher early in the year, but no rocket-like rise has been seen. This remains tied to cautious demand in the global consumer sector. Consumers have been paying higher interest costs and defence-related expenses, while the savings rate has continued to rise. - Nokia and the Technology Sector.

This time, Nokia surprised the market by exceeding expectations. In particular, optical cables used in data centre data transmission grew rapidly, and under new management, Nokia delivered a clearly positive message to the market. Nokia’s share price has already doubled this year, meaning that considerable expectations for future growth have been priced in over a short period. On the other hand, Nokia’s position in certain parts of the network is strong, and US peers such as Ciena are valued at entirely different multiples than Nokia. Of course, that competitor is more focused specifically on the data transmission networks needed in data centres.

Among smaller technology companies such as Vaisala, Bittium and cybersecurity companies, the news was also fairly positive, although largely in line with analyst expectations. - Small Caps.

In terms of share price performance, smaller companies by market capitalisation have once again been clearly overshadowed by large caps this year. There have been individual rockets, such as Saga Furs, formerly Turkistuottajat, which improved its earnings, silver mining company Sotkamo Silver, and gold mining company Endomines. All of these significantly improved their earnings compared with last year, although the mining companies at least face significant investments to secure further material.

Although share price performance has not exactly pampered these small companies, earnings development was quite positive for many of them, including Harvia, Marimekko, QT and Exel Composites. Many others could also be mentioned, but overall, the small-cap earnings season went rather well. That said, there is significant polarisation, and some companies had to raise capital through “forced issues” to strengthen their financial position. Examples include Faron, Bioretec, Eezy and, most recently, Summa Defence, which reported issues with its financing.

The Q1/2026 earnings season is effectively over on the Helsinki Stock Exchange. Overall, it went quite well. There were relatively few major disappointments, with Tokmanni, which is wrestling with an acquisition, being one such example. In general, results met or slightly exceeded expectations.

In the domestic market, early signs of recovery can be observed, as consumers are finally daring to put slightly more money to work. At the same time, export demand is in reasonably good shape, and we have also recently received several positive investment announcements in Finland. Although our listed companies operate in the global economy and the Finnish national economy is not of decisive importance to them, a recovery in the domestic market would also matter, especially for our small-cap universe.

All in all, the year started well from an earnings perspective. Guidance held, and there were no major dramatic disappointments.

This is a good basis from which to continue towards a sunny summer.

18 May 2026

Mika Heikkilä

Portfolio Manager

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Would you like to receive our latest writings directly in your inbox?

Subscribe to our newsletter. We share our views on investing and current market themes.