Record Number of Tender Offers in Scandinavia – Early Signs of Optimism in Small Caps

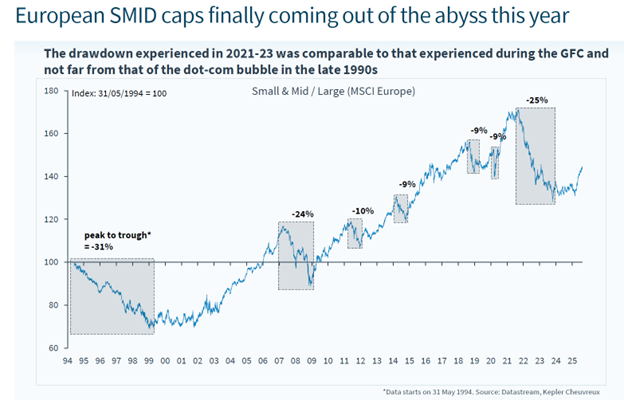

Small caps have faced an almost historically difficult period in recent years, largely regardless of geography, particularly relative to large caps. As shown in the figure below, one has to go all the way back to the 1990s to find a period in which European small caps have performed as weakly relative to large caps.

Recently, however, there have been some early signs of optimism in small caps as well, as valuation levels in many areas have fallen very low while the economic outlook is showing modest signs of improvement. At the same time, it is worth noting that share price performance has been better among somewhat larger small-cap companies than among the very smallest companies, i.e. micro caps, where performance has been more modest.

In investment markets, it is fairly typical that when market sentiment improves, capital starts to move down the market-cap spectrum: first into larger small caps and then gradually further down, with micro caps usually the last in line. Once markets begin to take an interest in micro caps again, the moves can be quite significant, partly due to limited supply.

Figure 1. Performance of European small and mid-cap equities relative to large caps.

Source: Kepler Cheuvreux and Datastream

The Small- and Micro-Cap Market in Scandinavia

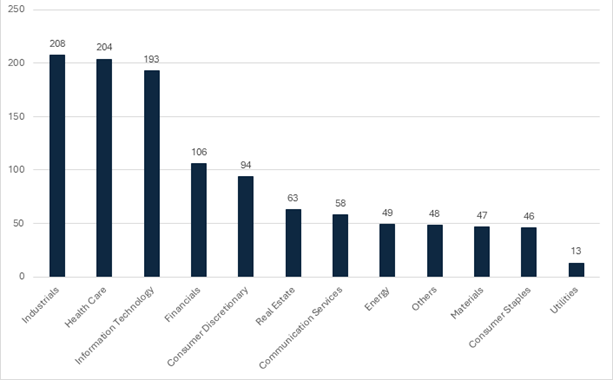

The listed small-cap markets in Scandinavia, defined here as companies with a market capitalisation below EUR 1 billion, form one of the world’s most interesting investment universes in terms of both the number of companies and overall attractiveness, offering as many as 1,129 listed companies.

The largest sectors are industrials, healthcare and information technology. Each of these sectors includes roughly 200 companies, and Sweden in particular has a large number of healthcare and information technology companies. Sweden is by far the largest small-cap market in Scandinavia, with as much as 70% of all small-cap companies listed in Sweden, either on OMX Stockholm or on other marketplaces such as First North.

Figure 2. Number of Scandinavian small-cap companies by sector

Source: Bloomberg and Proprius Partners

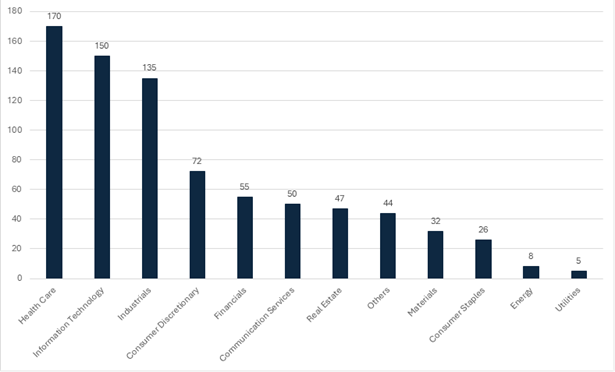

Figure 3. Number of Swedish small-cap companies by sector

Source: Bloomberg and Proprius Partners

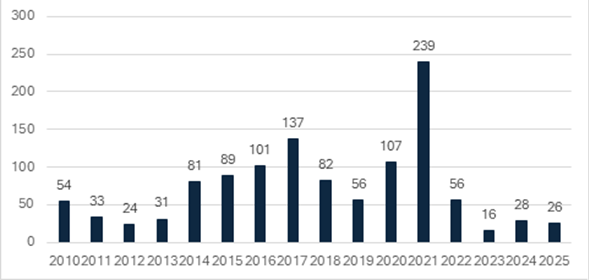

The IPO Market Remains Frozen

IPO activity is generally considered a kind of risk sentiment indicator in equity markets. When risk sentiment is strong, many companies list on the stock exchange; conversely, when investors are cautious, the number of IPOs remains low.

The last true golden age for IPOs was in 2021, when as many as 239 companies listed on Scandinavian exchanges. Since then, IPO activity has been fairly limited, at around 30 listings per year. In fact, one has to go back almost 15 years, to the aftermath of the financial crisis and the euro crisis, to find a period when IPO activity was as low as it is today (Figure 4).

That said, this autumn has shown some modest signs of increasing IPO activity, and several listings have gone rather well, also performing favourably as listed companies. It may therefore be that this part of the market is gradually starting to recover as well.

Figure 4. Number of IPOs in Scandinavia in 2010–2025

Source: FactSet and Proprius Partners

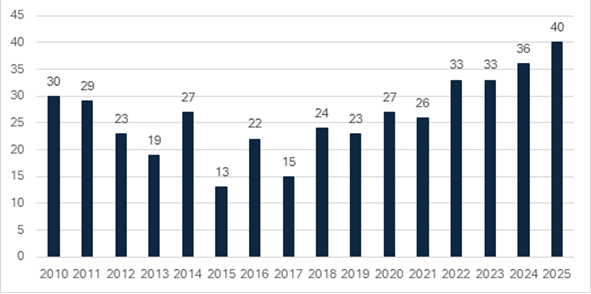

Record Public Tender Offers – As Many as 40 Companies Have Received Offers This Year

While IPO activity has been low in recent years, tender offers for listed companies have been all the more active. In a 15-year comparison, recent years have been very busy, and the current year will be the most active of the entire period.

This likely says something about the fact that both industrial buyers and private equity investors see a large number of attractively priced, high-quality companies available in the listed market. In other words, investors now appear to view valuation levels in Scandinavian stock markets as such that they prefer to acquire listed companies at a premium rather than list new ones.

This could support the view that the current risk/reward profile in listed small caps is attractive. Proprius Partners Micro Scandinavia has also already received five tender offers during its just over two-year operating history.

Figure 5. Number of public tender offers in Scandinavia in 2010–2025

Source: FactSet and Proprius Partners

The Swedish Economy Is Recovering, with GDP Forecast to Grow by Around 2.5% in 2026

In 2026, clear signs of recovery are visible in the Swedish economy. Consumer confidence is improving, and households’ real disposable income is forecast to grow by as much as 4% this year, which would represent a significant increase compared with the previous few years.

Households are being supported through tax cuts. For example, the VAT rate on food will be reduced from 12% to 6% from 1 April 2026 until the end of 2027. Swedish GDP is expected to grow by around 2.4% next year according to the Bloomberg consensus, and forecasts have recently been revised upwards. For instance, the Riksbank recently raised its forecast to 2.9%. The manufacturing PMI rose to 55.3 in December.

Strong Growth Forecast for Micro Scandinavia Companies in 2026

Approximately 87% of Proprius Micro Scandinavia’s investments are listed in Sweden, and the largest sectors in the portfolio are information technology, at around 35%, and healthcare, at around 31%.

Recently, we have slightly increased our exposure to consumer goods companies, based on the rather positive outlook for the Swedish economy this year. According to Bloomberg consensus estimates, Micro Scandinavia’s portfolio companies are expected to grow revenue by around 12% at the median level this year and earnings by as much as 36% at the median level.

At this stage, however, we remain somewhat cautious regarding these forecasts, as estimates have also had to be revised down during the year in previous years. That said, the positive momentum in the Swedish economy this year may support the business outlook for these companies, as small caps on average tend to be more domestically oriented than large caps.

A stronger economic backdrop may also translate into increased investor interest in small and micro-cap companies. At the beginning of January, we will therefore spend three days in Copenhagen at our partner’s seminar, meeting both existing portfolio companies and potential new investment opportunities.

We look to 2026 with confidence.

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa