Selectivity Is Key as Finnish Large-Cap Stocks Have Rallied — Earnings Growth Is Needed, or Disappointments May Follow

***Let us begin with a brief announcement. Proprius Partners’ assets under management have reached EUR 200 million. We are proud and grateful that you have helped make this milestone possible. We will continue to do our utmost to remain worthy of your trust.***

After 2024, many investors in Finnish equities had all but thrown in the towel. The US equity market once again posted impressive gains, while Finland continued to tread water, and the journey for small and mid-sized companies in particular was painfully difficult. At the same time, a great deal of air had been taken out of the prices of many Finnish equities.

This created a setup few dared to even dream of: in 2025, the Helsinki equity market, as measured by the OMX Helsinki Cap GI, rose a handsome 35.3% including dividends, driven especially by large caps.

Following last year’s rally, it is worth pausing to assess what the valuation level of the Helsinki market looks like after the first steps of 2026, as many stocks have seen significant moves — mostly upwards.

Figure 1. Balance sheet-based valuation (P/B) of the OMX Helsinki Cap Index on the right axis and forward earnings-based valuation (P/E) on the left axis. Source: Bloomberg, 9 January 2026.

In addition to Figure 1, here are a few valuation metrics in numbers. According to Bloomberg, as of 9 January 2026, the forecast P/E multiple for the OMX Helsinki Cap Index is approximately 21.1x for 2025, 17.2x for 2026 and 15.0x for 2027. In other words, earnings per share are expected to grow by around 23.2% this year and around 14.1% next year. The P/B multiple is approximately 2.2x, as Figure 1 shows, and is gradually approaching 2x on a forward-looking basis. Dividend yield forecasts are in the range of 3.6–4.1% for dividends paid in respect of 2025–2027.

Balance sheet-based valuation is, in the context of recent years, more on the high side than the low side — although valuations had admittedly been low in recent years. Dividend yields have also been compressed to relatively modest levels by Helsinki standards. Forward P/E multiples are reasonable when one considers how weak the earnings power of many Finnish large caps has been in recent years, such as Neste and the forest companies.

In absolute terms, earnings growth expectations are demanding and hold up even in an international comparison. If the growth forecasts are met, the situation looks quite good. At the index level, however, it has typically been more common for early-year fantasies to fade and forecasts to be revised down over the course of the year.

In Helsinki, the impact of a few large companies on the aggregate earnings pool is naturally very significant, and many would argue that following the entire Helsinki market at index level is almost absurd. On the other hand, one could increasingly make the same argument about the S&P 500 as well, given how a handful of technology companies now dominate that index.

For Helsinki, however, the conclusion is clear: valuations have risen significantly, and earnings growth needs to be delivered. Otherwise, future returns at the index level are likely to remain modest.

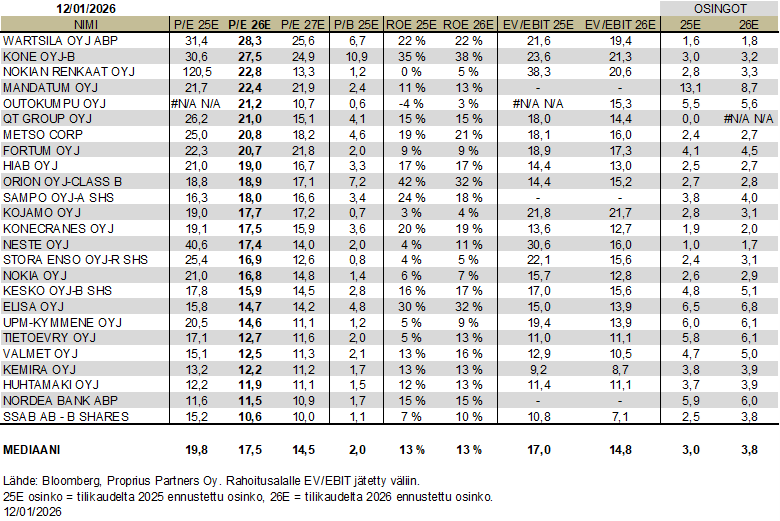

Figure 2. Valuation levels of OMX Helsinki 25 constituents ranked by forecast 2026 P/E multiple. Source: Bloomberg, 12 January 2026.

Among the “most expensive” names, Wärtsilä, which has benefited from the data centre boom, is expected to deliver EPS growth of around 10–11% and revenue growth of roughly 7% in both 2026 and 2027. Kone is also expected to deliver earnings growth of 10–11%, but with somewhat lower revenue growth of around 4–6% over the same periods.

Mandatum is not priced for earnings growth, but at least at the time of writing, the investment case rests more on capital distributions — a story that has resonated strongly with Finnish investors. Nokian Tyres, in turn, is ramping up its factory in Romania, which is why the 2026 multiples still look demanding, although an improvement should be on the cards by any reasonable assessment.

Let us return briefly to the valuations of Kone and Wärtsilä, as both are widely seen as belonging to the absolute elite of Finnish listed industrial companies. Earnings growth of around 10% is, of course, a perfectly respectable figure. However, the earnings-based valuation alone suggests that, at least in a historical context, these companies cannot currently be bought cheaply for one’s portfolio.

The forecast P/E multiples for 2025 are above 30x, and even looking forward to this year, both are still around 28x. In return for these high P/E multiples, investors do get excellent returns on equity and strong balance sheets. Given the companies’ substantial net cash positions, it may actually make more sense to look at EV/EBIT multiples, which are more moderate than the P/E multiples for these companies.

Still, if one relates P/E multiples to earnings growth — the PEG ratio — one ends up at roughly 3x. That multiple certainly does not scream “buy”, especially for such established, large and stable Finnish companies — quite the opposite.

This is also supported by Figure 3, which illustrates the development of Kone’s and Wärtsilä’s EV/Sales multiples over the past 20 years. In Kone’s defence, excluding the extraordinary enthusiasm during the COVID period, the company’s EV/Sales multiple has remained fairly stable at around 2.0–2.5x since the 2010s, so the current multiple is not dramatically high for the company. Wärtsilä’s multiple, by contrast, is strikingly high at the moment, and its history has been clearly more volatile than Kone’s. At the same time, Wärtsilä’s outlook is better than it has been for a long time. Hopefully data centre orders — and other orders as well — continue to flow at a healthy pace.

Figure 3. Development of Kone’s and Wärtsilä’s EV/Sales multiples over the past 20 years. Source: Bloomberg, 12 January 2026.

The purpose here is not to go through the valuation of every OMX Helsinki 25 company in detail, but rather to support the idea that a fair amount of optimism is already priced into some stocks. Naturally, it will not surprise readers that a portfolio manager argues in favour of selectivity in stock picking.

Last year, however, that would not have been the obvious strategy, because most picks outside the large-cap segment in Helsinki underperformed the broader market. An index product would very likely have produced a better result than one’s own analysis and legwork.

Figure 4 further shows how badly small and mid-sized companies in Finland have lagged large caps over the past five years. As large caps have now become more expensive in many areas, it is likely that an increasing number of investors will, at some point, begin to take interest in the return opportunities offered by smaller companies as well. Last year already saw several sharp rallies, including in Endomines, Bittium, WithSecure, SSH and Verkkokauppa.

Figure 4. Performance of the OMX Helsinki 25 Index, OMX Helsinki Small Cap GI and OMX Helsinki Mid Cap GI over the past five years. Source: Bloomberg, 12 January 2026.

At Proprius Partners, we continue to invest in larger companies through a value and dividend philosophy in the Proprius Partners Arvo Suomi non-UCITS fund. Based on that philosophy, we make our own judgments about what we are willing to pay for each company. Kone and Wärtsilä are not currently trading at multiples that we find acceptable, but that does not mean they cannot continue to rise.

The Proprius Partners Micro Finland non-UCITS fund, which invests in small and mid-sized companies, focuses on companies with a market capitalisation below EUR 1 billion. We have already gathered EUR 54 million into this fund during a period when Finnish small and mid-sized listed companies have been deeply out of favour.

The work continues in both Arvo Suomi and Micro Finland — whether our strategies are in fashion at any given moment or not.

Of the companies mentioned in this text, Arvo Suomi held Mandatum shares with a weighting of just over 1% at the time of writing. We bought the stock back into the portfolio when Altor reduced its holding through a placement in the summer of 2025. WithSecure was held in the Micro Finland fund until the tender offer. Outside the companies mentioned in the text, our funds hold several companies from the group shown in Figure 2.

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa