Buy the Dip – Finland Earnings Season Review Q4/2025

2025 was an excellent year for companies listed on the Helsinki Stock Exchange. Share prices rose strongly, particularly toward the end of the year, pushing valuation multiples higher and making the Q4/2025 earnings season especially closely watched. How did companies perform in the final quarter? How were results affected by geopolitical developments? And, most importantly, what did 2026 guidance look like?

Week 8 marks the start of the first winter holidays in Finland, and most companies time their earnings releases for the preceding week. As a result, the mornings leading into the ski holiday period were packed with reports to read and models to update. Even though information is being processed and compared faster than ever, the market’s initial reaction in the morning – and often throughout the reporting day – can still appear extreme relative to the information released.

Every investor naturally follows their own strategy, but at Proprius Partners, as long-term investors, we prefer to first look, study and spend at least some time analyzing and reflecting on what an earnings report is actually telling us. Based on the Finnish Q4 earnings season, our key takeaway became “buy the dip”, as so many share price reactions were surprisingly sharp on the downside even when the actual release was largely in line with expectations or even encouraging.

When looking at the Helsinki market as a whole, it is important to bear in mind the structure of the market. The aggregate earnings figure can be heavily influenced by just a few large companies, so it usually pays to look under the bonnet to understand what is actually driving earnings changes or deviations. Such mega-caps on the Helsinki exchange include Nordea, Nokia and Neste, among others. Aggregate changes should therefore always be treated with care. In the following, I use material prepared by our partner OP Markets; at the time of compilation, 78% of the companies under OP’s coverage were included in the analysis.

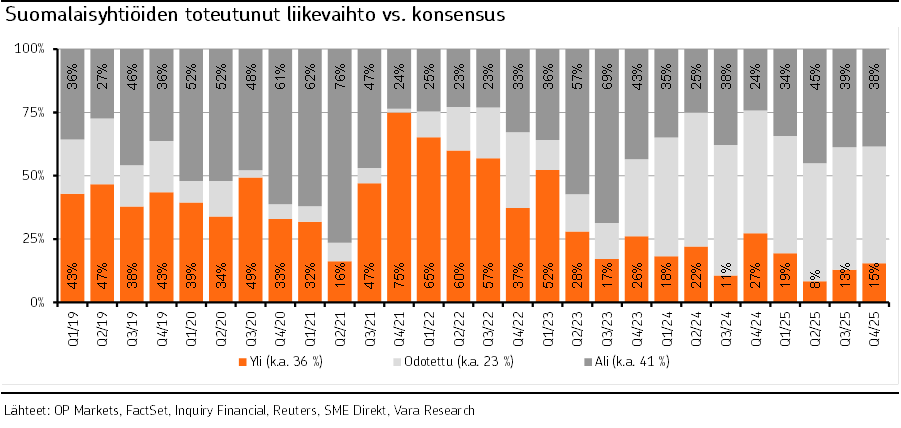

There were very few positive surprises on the revenue line. One reason for this was the pronounced weakening of the US dollar during 2025, the effects of which become visible over time as currency hedges roll off – and those roll-offs are difficult for analysts to estimate precisely. In other words, listed companies continued along the expected growth path toward year-end, but without delivering major upside surprises.

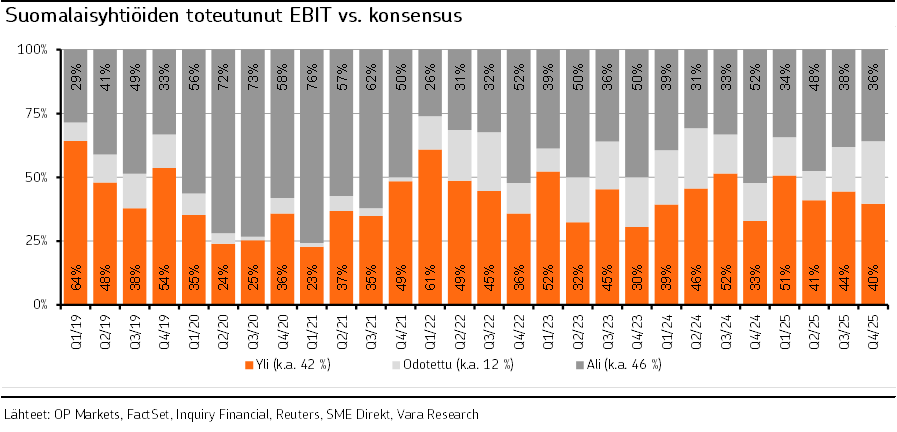

On the EBIT line, however, positive surprises continued, as a significant share of companies still beat expectations. This speaks to the operational efficiency of Finnish companies, which remains underpinned by strict financial discipline. Looking ahead, it is worth remembering that if revenues were to start accelerating, the earnings impact could be very significant, because companies have spent recent years streamlining themselves into lean profit-generating machines.

Dividend growth appears to be slowing, which may reflect the discussion that began last autumn around encouraging companies to invest in growth rather than simply distribute ever-rising dividends. Dividend yields remain high, but it would be a welcome change if more capital were directed toward future growth. That, of course, requires a supportive market backdrop. Share buybacks also seem to be part of the toolbox for a surprisingly large number of companies.

To sum up: revenues broadly in line with expectations, earnings showing a slight positive bias, and dividends still at elevated levels. That was the overall picture of the Q4/2025 earnings season.

Figure 1. Revenues relative to expectations, source OP Markets.

Figure 2. EBIT relative to expectations, source OP Markets.

Capital Goods. The leading sector on the Helsinki Stock Exchange for a long time now, and once again it did not disappoint in the bigger picture. Strong share price performers Wärtsilä, Konecranes and Metso delivered earnings in line with or slightly above expectations, while new orders were strong across the board. The companies are benefiting from somewhat different structural themes: Wärtsilä from energy solutions for data centres, Metso from rising metal prices, and Konecranes from a broader pickup in investment activity.

In all three cases, the initial share price reaction was down, but after a delay of a few days, the stocks recovered back to – or in some cases above – their pre-result levels. These companies’ valuation levels require growth, and as long as that growth continues to materialise, there is room for further upside. But one needs to stay alert: with expectations high, volatility will remain a feature.

Kone, Valmet and Hiab were more in the slower-growth bucket, as expected. Of these, only Hiab came in slightly below expectations, but even there the outlook remained fairly solid. Valmet’s valuation, however, is on a completely different level compared to the other capital goods names, and Proprius Partners’ Arvo Suomi fund added to Valmet during the reporting season.

Overall, the capital goods sector handled elevated expectations well and broadly confirmed the market’s assumption that growth will continue this year. A good performance overall.

Forest Sector. There is light at the end of the tunnel. 2025 ended somewhat better than the low expectations implied. Guidance, however, remained cautious. Packaging materials continue to suffer from excess capacity, US tariffs are weighing on demand, and a weaker dollar is pressuring margins. This has particularly hurt Metsä Board (which we do not own in our funds) and, to some extent, also Stora Enso.

UPM is more directly exposed to pulp prices, which began to recover gradually toward the end of the year. A clear earnings improvement is expected this year versus last, and if pulp prices continue to rise, the improvement could be substantial. End demand for pulp ultimately comes from consumers, who remain cautious.

If one also includes Huhtamäki in this sector discussion – it uses cartonboard rather than producing it – the same weakness in global consumer demand is visible there as well, and with it muted growth. In relation to current profitability, this is reflected in very modest valuation multiples, which has at least certainly caught the attention of value investors in Huhtamäki’s case.

A global pickup in consumer demand would be one of the most positive surprises this year and would benefit many companies on the Helsinki exchange. For now, however, the consumer remains rather cautious, partly because of geopolitical risks.

Banks and Financials. This sector continues to run like a train – stable beyond stable. Nordea, Aktia, Sampo and the asset managers: there has been little real drama here. Real estate remains a drag for those companies with meaningful exposure to it. Credit losses for the banks remain negligible, which unfortunately also says something about the current level of risk-taking in the Finnish economy.

The Finnish economy is now in its third year of recession, yet banks’ credit losses are still almost non-existent. Banks have been extremely successful in selecting risks, while at the same time Finnish economic growth remains deeply frozen, as credit is extended only to the safest of cases – cases that often do not even need bank financing. For equity investors, however, these are attractive businesses: profitability is solid, dividends are generous and valuations are still quite modest.

Sampo saw a strange sell-off when US insurer Lemonade promised 50% lower comprehensive motor insurance premiums for Tesla self-driving cars. Given Nordic winter conditions, I would like to see the day when fully autonomous vehicles are widespread in the Nordics and insurance premiums are halved accordingly. It is also worth remembering that Sampo, too, is making use of AI in its future insurance offerings. In our view, this was once again a good opportunity to add to this Nordic insurance giant, whose earnings, once again, did not disappoint – steady execution across the board.

Nokia. A new chapter is opening. Nokia did not disappoint in Q4; on the contrary, it slightly beat expectations. But like many others, it guided cautiously and brought market expectations – read: analyst expectations – down a bit. That, in turn, leaves room to surprise positively as the year progresses.

Nokia is beginning to benefit from stronger growth driven by AI investment, even if it still cannot be described as a high-growth company. But valuation is only slightly elevated, and if it gradually achieves its growth targets, one can expect earnings to improve. This was a classic “buy the dip” stock this reporting season.

Figure 3. Nokia share price development around the earnings release (results on 29 January 2026). The dip recovered within a few days, and the stock has since moved clearly higher (at the time of writing, EUR 6.40). Source: Bloomberg.

Energy: Fortum and Neste. Fortum had hedged electricity prices well in advance, and as a result its earnings were broadly as expected, even though the market does not currently expect power prices a few years out to revisit the sort of spikes seen this winter.

What has been supporting the share price, however, is simply the growing electricity consumption of data centres, and especially US investor interest in listed companies that produce power through, among other things, nuclear energy. Their view is that electricity prices must rise if demand increases sharply. Fortum, for its part, is currently saying that at today’s power prices, there is little incentive to make new investments. This stand-off, in the context of ever more data centres coming online, clearly creates upward pressure on electricity prices – which would then spur investment, which would then bring prices back down, and so on.

A very interesting dynamic, but one on which it is currently difficult to form a highly informed view – other than that the role of energy is becoming increasingly important across economies.

Neste, meanwhile, clearly beat expectations for the end of the year, with European demand for renewable biofuels especially strong. Guidance for this year was softer due to refinery maintenance shutdowns and challenges in the US market, but the nightmare of last year is now clearly behind it. In 2027, the Rotterdam refinery expansion will be completed, significantly increasing Neste’s capacity.

Small Caps. This is where things really happen. Stocks such as Sotkamo Silver and Endomines – one-mine stories – had already rallied strongly ahead of results. After earnings, the situation generally calmed down somewhat, as valuation multiples had run too far ahead and realistic guidance brought expectations back to earth. That was the case, for example, with SSH, QPR Software and Kempower.

This group has seen very sharp share price moves whenever there has been anything genuinely surprising. Faron and Bioretec, both of which announced share issues, fell more than 50% on those announcements. At present, the stock market expects small caps to remain broadly on track with their growth and earnings targets – and it hates uncertainty.

A good example is recently listed Framery: an approximately in-line result still sent the share price down more than 10% on the day. I could continue with countless such examples, but investors focused on small caps know them well already, and for the unitholders of Proprius Partners Micro Finland, assessing exactly these situations is quite literally our day job.

These sharp moves reflect the thin liquidity in the space and the importance of that liquidity for short-term price moves. There may be short-term traders in these names even though the liquidity of the stock does not really permit fast trading. That is why following small-cap price movements sometimes requires a strong stomach – and perhaps a good skiing session on a cold winter day in the middle of earnings season.

Summary. There were no major surprises at the revenue level. The top line continues to grow at a fairly moderate pace. Large companies remain in good earnings shape and offer the potential for stronger revenue growth ahead.

In small caps, however, share price moves were dramatic. In some cases, they represented a return to reality; in others, they detached completely from the reality of the earnings report itself. For investors, that means reading, listening and doing the work. Liquidity is already decent in large caps; in small caps it remains poor.

From the perspective of Proprius’ Finnish equity funds, Arvo Suomi was able to further strengthen its portfolio of cheaper expected-return opportunities at very modest multiples, with the expected dividend yield still hovering around 5%. In small caps, we were prepared to add to companies whose businesses were progressing in line with plan and delivering results. And that is exactly what happened: to our surprise, after initial 10% price drops, we were able to buy many of our holdings at levels lower than we had expected. “Buy the dip” increasingly became the theme in many names.

That, of course, requires continued global growth and, in particular, a recovery in the European economy. If that materialises, it will also have positive spillover effects on Finland, and especially on the small-cap market here.

The Helsinki market is currently trading at roughly 17.9x P/E for this year and 15.4x for next year. That means we are somewhat above historical levels for this year, but as forecasts materialise over the course of the year, the market should move back below average. The market is expecting around 16% earnings growth on average, with Neste, Nokia and the forest companies explaining a large share of that, given how weak the early part of last year was.

Our Arvo Suomi fund is currently trading at about 15x P/E on this year’s estimates, which leaves us roughly 20% below the broader market. That gives our earnings growth expectations a good cushion in the form of low valuation, should something disappoint.

Despite all the geopolitical news flow, the market outlook is fundamentally still fairly satisfactory, and we expect positive news from our holdings during the year. That is why “buy the dip” was the theme of this reporting season.

Wishing you sunshine and good skiing conditions,

Portfolio Manager Heikkilä

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa