Earnings Season Closed a Difficult Year in Finland and Offered Hopes of Better Times Ahead

The text should not be interpreted as investment advice or an investment recommendation.

The Q4/2024 earnings season is now more or less over. In general, it can be said that the season was not particularly dramatic: there were no broad-based disappointments, and there were even some developments on the positive side. Of course, a few companies delivered severe disappointments, partly due to their own execution. But in the big picture, the earnings season met expectations, which, after last year’s weak share price performance, can clearly be seen as a positive outcome.

Roughly speaking, around 80% of the largest companies met or exceeded revenue expectations. This was likely helped to some extent by the weaker euro against the US dollar, which supports our export companies. At the earnings level, the picture was not quite as positive: just over half of companies met or exceeded earnings expectations, while slightly less than half fell short. Still, the fact that there were no massive earnings disappointments was enough to lift the Helsinki Stock Exchange to the top of the Western equity markets early in the year, supported by low valuations.

Let us go through the positives, negatives and oddities of the Helsinki earnings season by group.

Positives:

- Capital goods. Overall, both the earnings power of the capital goods companies and, above all, the volume of new orders were among the most positive features of this earnings season. This reflects both reasonable momentum in the global economy and the capabilities of Finnish engineering companies, as orders continue to come in from around the world. Wärtsilä and Konecranes were particularly convincing with their new orders. Kone is recovering from the slowdown in Chinese construction, supported by maintenance and modernisation, although growth remains modest. Cargotec, Kalmar, Metso and Valmet were all broadly in line with expectations, so there were few disappointments in this sector.

- Banks and financials. Earnings remained very strong despite the slight downward trend in interest rates. Nordea’s result was excellent, and given that the valuation is cheap on an earnings basis, it is no surprise that the share price continued to rise after the result. Sampo also delivered a very strong result, while at the same time showing signs of placing more emphasis on growth. Among smaller banks and asset managers, Aktia delivered a slightly better-than-expected result, as did Taaleri. Evli, CapMan and UB reported results broadly in line with expectations. Only asset managers linked to real estate, such as eQ, fell clearly short of expectations. Oma Säästöpankki’s result continued to be weighed down by write-downs, which highlighted last year the importance of strict lending discipline, as credit losses among the large banks remained surprisingly low. Overall, this sector also belongs in the positive column, and large dividends are again expected for shareholders at the spring annual general meetings.

- Nokia and the technology sector. For the first time in a while, Nokia delivered a reassuring interim result. Considering that the guidance for Q4 was quite demanding, the performance was all the better. Nokia is gradually getting its business back on track after the lost AT&T deals. A new CEO and the completion of the Infinera transaction support the view that growth may improve. Among other technology companies, QT and Vaisala either already delivered excellent results or issued strong guidance. The technology sector is therefore gradually improving, although one would hope it were clearly larger and broader on the Helsinki Stock Exchange.

Negatives:

- Neste. In practice, the renewable products margin, which had already been lowered four times during the year, fell to rock-bottom levels by the end of the year. Neste’s result missed all expectations, and the steepness of the deterioration surprised both company management and investors. Globally, more capacity is coming into renewable products, and political pressure to reduce distribution obligations has continued. At the same time, Neste’s own execution has also been weak. There have been shortcomings in refinery operations, the Rotterdam refinery is behind schedule and will cost significantly more than expected, and a devastating fire occurred last year at the joint venture in the United States. All of this caused the result to collapse, pushed the share price down and led to a change in Neste’s management. Neste’s future lies in aviation fuels, where political decisions should significantly increase demand by 2030, but unfortunately that is still a long way off.

- Nokian Tyres. The company’s Q4 guidance was demanding, and the result for this most important quarter ended up being roughly half of what was expected. To meet reasonably good demand, Nokian Tyres used a large amount of subcontracting, which was visible in margins. This situation will ease when the new Romanian factory starts up next autumn. More worrying was the very weak profitability of the US factory in Dayton, which has already been operating for several years. The shift from the Russian market to the Central European tyre market is not easy, as Nokian Tyres’ brand faces much tougher competition in Europe. In our view, the company absolutely should have issued a profit warning, but for some reason it did not. In addition, the dividend cut was a clear surprise relative to market expectations and previous communication, even though the decision itself was probably entirely correct.

- Construction companies. Construction remains completely frozen in new housing. The redemption problems of open-ended real estate funds make the situation even worse, meaning that there is simply no demand for building small apartments. Projects started this year will only be completed in 2026, so this year too will mainly consist of low-margin contracting work for the large listed construction companies.

Other Observations from the Earnings Season:

- Small companies. There was a bit of everything. The worst was clearly behind us, and where the customer base is stable, a certain degree of earnings resilience has been found. For reasons of space, I will not go through every company line by line, but positive surprises included at least restaurant company NoHo, Alma, Exel Composites and Detection Technology. Clear disappointments, in turn, came from IT services companies such as Vincit, Gofore and a number of other small companies in the sector. Although digitalisation continues, customers are currently unwilling to order long-term projects, and government cost-saving measures are also having an impact.

- Healthcare companies were in strong earnings condition across the board. Terveystalo, Pihlajalinna and Orion all delivered strongly growing earnings, supported both by their own previous actions and by improving markets.

- Forest companies. UPM once again performed as the best in class, although it issued guidance that was slightly softer than expected. Stora Enso reported large write-downs, while Metsä Board was weighed down by weak pricing in packaging materials. The pulp price has continued to rise early in the year, so in that sense this large sector of the Helsinki Stock Exchange should continue its positive momentum.

Overall, the Q4/2024 earnings season in Finland did not disappoint. We got what we expected. This is definitely good news, because during the year we experienced clear disappointments on several occasions. With valuations low, the Helsinki Stock Exchange has risen by around 10% since the beginning of the year. I have also sensed more discussion around growth ambitions in company meetings, meaning the underlying tone has been cautiously optimistic.

Balance sheets are still mostly in good shape, although there are some very weak companies, especially among the smallest ones, and their future is a complete question mark. But as portfolio managers of Proprius’ Finnish equity funds, we feel reasonably satisfied with our portfolio companies. At these valuation levels, it is easy to justify owning the companies. We are also about to see the first IPO in a long time on the First North list. It will be interesting to see whether the improving situation also encourages broader capital market activity on the stock exchange. At least among smaller companies, that may well happen.

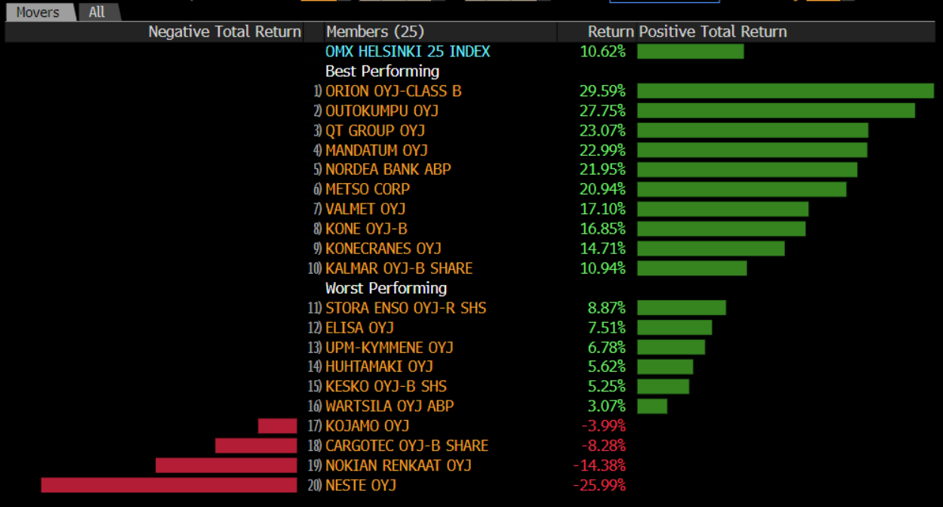

The charts below show the best- and worst-performing stocks in the OMX Helsinki Cap Index and OMX Helsinki 25 Index from the beginning of the year until the afternoon of 5 March 2025.

Source: Bloomberg.

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa