Market Letter X – Did We Come Here to Lose or to Win?

“We came,” Lampinen would say in Kummeli. In my view, Lampinen’s mentality captures modern investment culture rather well. These days, it often feels as if participating in markets has become more important than beating them. At least that is what the growth of passive assets relative to active assets would suggest. Or is passive investing simply superior to active investing?

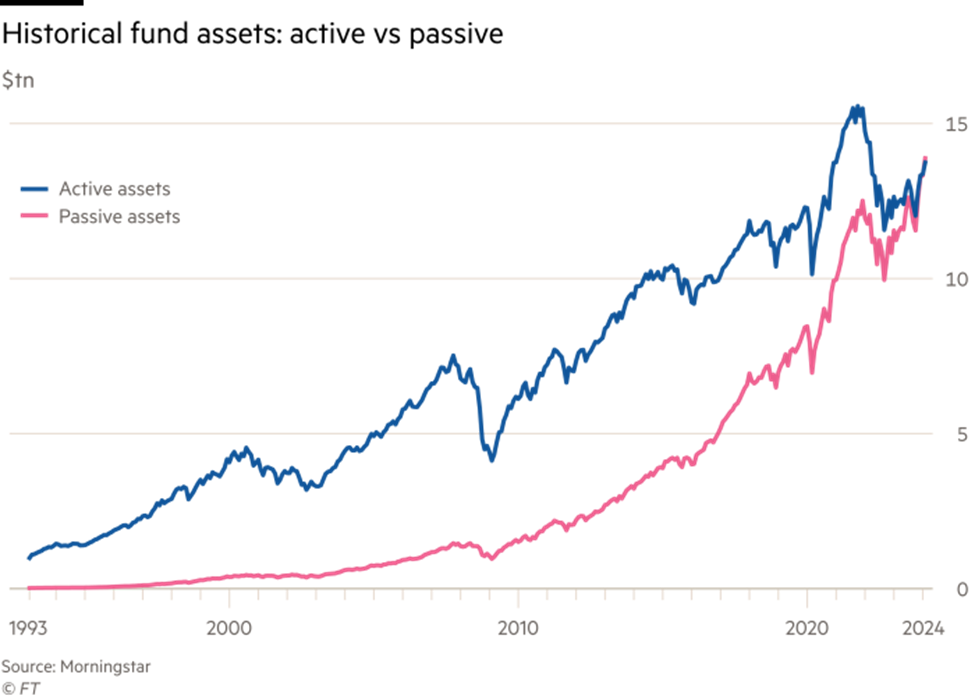

Figure 1: Assets invested in active and passive funds in the United States

Source: Financial Times

When active and passive portfolio management are framed against each other like this, many readers’ first thought is probably: “Oh no, here we go again.” And understandably so. The active versus passive investing debate is the most debated and researched topic in investing. Fortunately, I do not intend — nor do I need — to argue about that today. Passive portfolio management beats active portfolio management on average, full stop.

Instead, I intend to give you a motivational speech on why aiming for average is not enough — not in life, and not in investing. Because if it were enough, our society would soon find itself facing major problems. And as a counterweight to an increasingly polarised world, I will also try to argue that passive and active investment strategies can live in good harmony within your portfolio. In investing, as elsewhere, an open mind can produce the best outcome instead of joining an investment sect.

The active versus passive debate often suffers from the way people understand averages. Average life expectancy does not mean that one should start waiting for death at the age of 74. Nor do the average odds of making it to the NHL stop a child from practising towards their dream. Few of us stop studying after compulsory school either, even though people around the world spend, on average, 8.8 years in education. So why settle for average in investing?

One reason is the academic emphasis on market efficiency. The efficient market hypothesis makes economics easier to understand, but in reality markets are anything but perfect. The hypothesis is a useful starting point, not the final truth — economics is a social science, not a natural science.

Settling for average ultimately stems from the fear of losing. If the pain of loss weighs more heavily than the joy of winning, it is rational to choose passive, average returns. But if winning matters more, this realisation may guide you towards more active portfolio management.

Are You Investing to Participate in Economic Growth — or to Create It?

“Buying every available investment through an index fund, has little to do with real capital deployment… (it) provides cheap, broad exposure to economic growth. No harm in that, but it has nothing to do with wealth creation.”

Stuart Dunbar

Stuart Dunbar of the legendary investment firm Baillie Gifford reminds us that index investing offers cheap and broad exposure to economic growth, but it has little to do with actual wealth creation. At the heart of capitalism are competition and the efficient allocation of capital, yet in investing, settling for average and avoiding active risk have become more important than winning.

This mindset is highly damaging to the growth of welfare and productivity. Paradoxically, it also increases market inefficiency, as Cliff Asness has noted: index investing and the gamification of investing create more opportunities for disciplined, long-term active investing — but they also require the ability to withstand periods of underperformance.

The growing popularity of passive investing can therefore be partly explained by the periodic underperformance that is inherent in active portfolio management, and by the fact that these periods have become longer as market inefficiencies have increased. In addition, many institutional investors suffer from principal–agent problems. It is not enough for the portfolio manager — the agent — to withstand the periods of underperformance that come with active investing; the principal must also be able to tolerate them without perfect information.

As a result, investor type often plays a central role in determining how much active exposure is included in a portfolio. The temptation to build a portfolio passively around broad indices is great: if you go down with everyone else, no one will blame you for failing.

”Gross domestic product (GDP) is a simple average that tells us very little about the real underlying drivers of growth. It’s an output measure of what companies collectively do, not a precondition for growth investing.”

Stuart Dunbar

Baillie Gifford defines investing as the deliberate allocation of capital to real projects that create value by offering products or services for which there is demand. It is not merely about following share prices, but about long-term activity in which equity markets act as a tool: they make long-term investments liquid and allow risk to be shared among investors.

Active portfolio management is therefore not merely reacting to markets. It is a process aimed at creating real, long-term value:

- Identifying genuine investment opportunities that are not yet reflected in share prices, such as technological innovations, market changes or new business models

- Identifying companies with the potential to capture these opportunities and management teams capable of making the right decisions to build long-term value

- Acting as a high-quality owner: monitoring management decisions, supporting management, encouraging ambition and creating the conditions for long-term strategy execution

- Continuously assessing whether one’s view remains differentiated from that of other investors. If it no longer is, one looks for new, less well-known opportunities with greater long-term return potential

Successful active portfolio management therefore participates in creating economic growth, rather than merely benefiting from the work done by others. Successful active portfolio management is comparable to elite sports: it requires dedication, the accumulation of intellectual capital, refinement of strategy and finding the right playing field. Luck is always needed, but the objective is to minimise the role of chance and maximise the probability of success. And best of all, when it succeeds, it rewards both those who practise it and the surrounding society generously.

Who Succeeds in Active Portfolio Management?

The recipe for success in investing is specialisation. As in sports, a versatile decathlete does not beat a specialised sprinter over 100 metres. In the same way, broad-based asset managers often fall behind in individual markets where focused boutique managers and their funds excel.

These managers devote all their resources to a specific market. Their structure and incentives support the pursuit of outperformance, and research suggests that their strengths include decision-making independence, strategic focus, alignment of interests with clients and agility.

Since we ourselves are such a boutique, we naturally have strong views on what works and what does not in our own target markets.

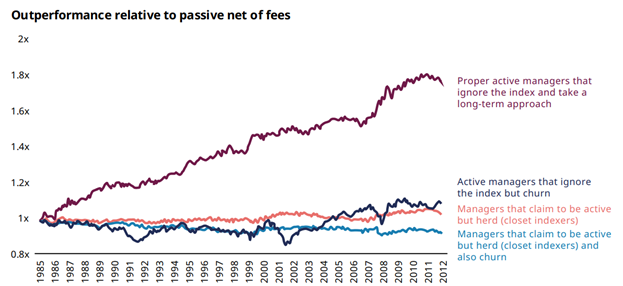

Figure 2: Performance of active equity funds, 1985–2012

Source: Baillie Gifford, Cremers & Pareek 2014

The figure shows what many already know to be true. Research indicates that the only fundamentally correct way to build an active equity portfolio for outperformance is to 1) take strong views and 2) trade as little as possible.

From the perspective of conviction, important metrics for investors are tracking error and active share. Manager selectors in listed equities should pay particular attention to active share, popularised through the work of Antti Petajisto. Active share tells us how much a fund’s holdings differ from its index. It is a fairly simple way to see immediately whether portfolio management is charging fees for replicating an index or genuinely taking a view.

Closet indexing ultimately benefits no one except perhaps the asset manager’s business. And maybe not even that.

So, in the end, the playbook for a manager selector in listed equities is simple:

- Does the portfolio manager take meaningful views? (active share & tracking error)

- Has taking those views added any value? (information ratio)

- Does the portfolio manager trade little within the fund? (low turnover)

- How well does the portfolio manager know their own market? (experience)

- Are there clear inefficiencies in the target market? (liquidity, analyst coverage)

A strong historical track record is often considered a good signal. I would, however, reduce its weighting somewhat in the evaluation. Its informational value is fairly weak. Past performance is certainly no guarantee of future returns.

”If you want to soar like an eagle in life, you can’t be flocking with the turkeys”

Warren Buffett

Active Strategies as Part of the Overall Portfolio

Strategic portfolio allocation has been approached both scientifically and pragmatically from many different angles and levels of asset allocation. The definition of active versus passive allocation, however, has received considerably less attention. Let us therefore offer a few thoughts on that question.

So far, we have discussed the importance and opportunities of active portfolio management. Active and passive management do not, however, need to be mutually exclusive. They complement each other. That is why we will next also present arguments for why a portfolio should include a passive component.

Passive investing provides cost-efficient access to the long-term return of the market, typically around 4–7% p.a. in nominal terms depending on asset allocation. If market returns are not enough, or if you do not want to be fully market-dependent, additional return can be sought by increasing active risk.

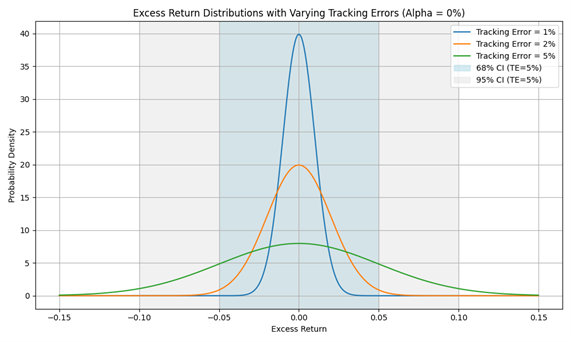

Active risk, or tracking error, measures the deviation of a portfolio’s returns from the market and therefore its alpha potential — but also the risk of losing to the market.

A portfolio’s level of active risk reflects the investor’s preferences regarding winning:

- If the most important objective is to avoid losing to the market, active risk is kept very low, below 2%, and the emphasis is on index products.

- If average market returns are not enough, active risk is increased, either by investing with strong conviction oneself or through active managers.

Why does active risk matter? Put simply, if your portfolio does not differ from the market, you cannot generate outperformance. Active risk describes the volatility of the difference between your portfolio’s return and the benchmark. If that volatility does not exist, you will ultimately end up with the same outcome as the market, no matter how much work you put into your investment decisions.

Figure 3: Active risk is about the variance between the portfolio return and the benchmark return. The higher the active risk, the wider the dispersion of returns around market returns.

Source: Proprius Partnerss Partners)

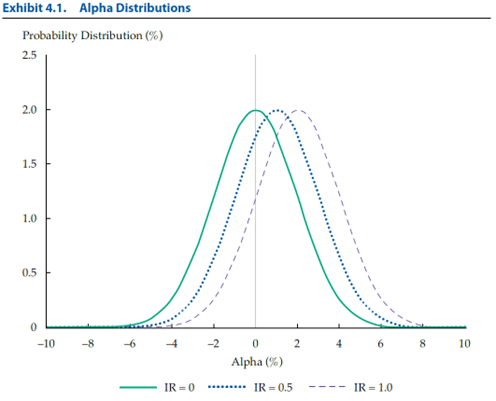

The importance of active risk can be illustrated through Richard Grinold’s Fundamental Law of Active Portfolio Management. According to it, excess return, or alpha, depends on both the skill of the portfolio manager (IC) and the number of independent investment decisions (BR):

IR = IC × √BR

where IR, or Information Ratio, measures excess return relative to active risk.

The formula tells us that the more often a portfolio manager’s views are correct, and the more independent views they take, the better the outcome. This links directly to active risk, or tracking error (TE), as expected excess return can be expressed as:

α = IR × TE

For investors, this means that expected excess return can be increased in two ways: by selecting managers or strategies with a high IR, or by increasing the portfolio’s active risk. In practice, active risk is easier to assess in advance than IR, which is based on historical returns.

Figure 4: Expected excess return at different Information Ratio levels and with 2% active risk. The Information Ratio shifts the expected excess return distribution, while active risk widens it.

Source: The Future of Investment Management, Ronald N. Kahn

Let us say that at this point you have defined your subjective preference for winning and would like to seek slightly better returns than the market, while still ensuring that if active management fails, the long-term market return has at least contributed positively to your portfolio.

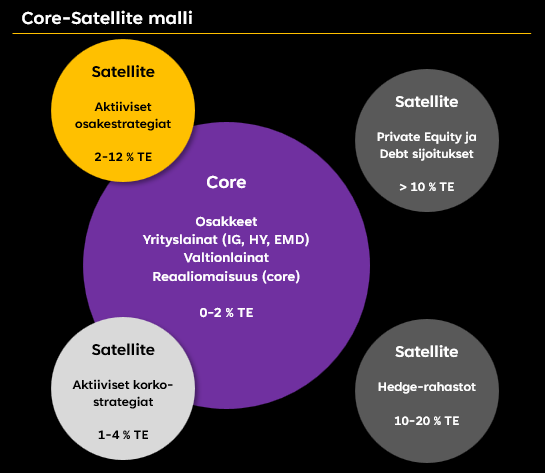

Would you then ask your generalist asset manager — your decathlete — who has built your portfolio using passive products to start making more active investment decisions and, in practice, enter the 100-metre sprint? No. Instead, you would seek the best of both worlds, passive and active investing, through a core–satellite model.

In the core–satellite model, cost-efficient index investments form the core of the portfolio, while active strategies act as satellites, providing additional return potential and diversification. The model gained prominence in the 2000s with the rise of ETFs and was further strengthened after the financial crisis, when it became clear that active strategies could behave differently from the market and therefore offer risk management benefits.

Figure 5: Archetype of the core–satellite model

Source: Proprius Partners

In the core–satellite model, the core provides broad, diversified market exposure aligned with the investor’s risk level, for example across equities, fixed income and liquid real assets. Its role is to deliver the long-term market return and preserve portfolio liquidity. This part of the portfolio represents the specialist competence of generalist asset managers: a broad range of instruments across asset classes and markets, as well as professional portfolio-level analysis and advice, which create value for investors.

The satellites, in turn, provide sources of alpha, increase active risk and may include illiquid asset classes such as private equity, where returns are based on active portfolio management and a long investment horizon. As discussed earlier, these active strategies require specialised boutiques focused on a specific asset class and market in order to succeed. That is what we at Proprius Partners represent.

The investor’s choice between the core and satellites depends on their objectives:

- If the most important objective is to avoid losing to the market, active risk is kept moderate and the satellite allocation remains small.

- If the goal is outperformance and wealth creation, the satellite allocation can be significant, even at the expense of the core.

In practice, the level of activity is adjusted through both the relative weight of the core and satellites and the active risk level of the satellites. Which asset class and strategy should be used to bring activity into the portfolio depends on the core asset allocation, but above all on where you believe opportunities for outperformance exist — and where specialised boutiques capable of exploiting them can be found.

If you are an investor who swears by passive portfolio management, you can use a modest allocation to active satellites to bring diversification benefits and some excess return potential into your portfolio, without fearing that the overall portfolio will, over the long run, deviate significantly from general market performance. Often in this situation, active satellite investments are used in markets that cannot even be accessed passively. The Finnish small-cap market is one example.

If, on the other hand, you are, for example, a family office investor who swears by active portfolio management and is interested only in the absolute return of your investment activity rather than market return expectations or relative returns, you are likely to build your portfolio around satellites selected from different asset classes and boutiques. Even then, you can use a modest passive core to provide liquidity for future investment opportunities, while collecting market risk premia along the way.

Over the past decade, investors in both camps have allocated the active portions of listed-market portfolios to private equity, leaving listed markets largely to index products. Historical data has provided strong arguments for this approach, but as always, the easy excess returns in that market have now largely been eaten away. The average private equity manager barely reaches equity market returns. According to research, in the period after 2008, the median private equity return has barely kept pace with equity indices (Harvard Business School, Does the Case for Private Equity Still Hold?, 2024). The starting point is therefore already almost the same as in listed markets, yet investors are still willing to pay more for active management in private markets. This is likely a cognitive error that will be corrected over time.

The Recipe: Courage and Professional Pride

Investing has typically seen two religions: active and passive investing. We still have too few investors who are able to look at these opportunities side by side with an open mind as distinct approaches to investing. One is about allocating capital and creating growth; the other is about participating and staying on board.

One of the significant reasons behind the triumph of passive investing after the financial crisis has been the brainwashing that begins in lecture halls around the assumption of market efficiency. Economics, finance theory and the world in general become pleasantly understandable and simple when we assume that markets are efficient. On top of that, the average results of empirical studies support this view.

Yet anyone who has worked even a single day in financial markets understands that the world is not that perfect — not even close. In addition, average results conceal the full range of opportunities. The efficient market hypothesis is an extremely important foundation on the path to understanding this highly complex world, but it is not the final truth. Economics is not a natural science with universal truths; it is a social science dependent on time and place.

Active portfolio management is ultimately about competition, the most central feature of capitalism. It is about the desire to win and the fear of being average. There is nothing wrong with participating in global economic growth and belonging to the average group if one has nothing to offer in the competition.

But if capitalism does not function even at its source — in capital markets — then it is pointless to dream of the economic growth it is supposed to bring. The lack of economic growth in our home country, for example, has been widely discussed in recent years. In our view, one reason for this is the normalisation of average performance. Our welfare society has ensured that average performance is enough for many people, and as a result we have become lazy and lost the hunger to win.

Perhaps it is therefore high time to normalise competition instead, and to strive to win in every field. Including investing. In that way, markets serve us in their original purpose: increasing the productivity and standard of living of our society.

It is not yet too late to stop the triumph of passive investing. But it requires courage and professional pride from investors — qualities that have been missing. It requires investing in oneself in order to make informed capital allocation decisions that move society forward.

Investing in an ETF tracking the MSCI All Country World Index is giving up; it is throwing one’s own professional skill into the rubbish bin. Because if long-term active investors like us, who oversee capital allocation decisions, disappear from the listed market, the result will be capital market anarchy — and ultimately destruction.

”What we do in life, echoes in eternity”

Maximus Decimus Meridius, Gladiator-elokuva

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa