Market Letter XI – What now then?

“Että tuulet puhaltais, sadepilvet poistais, valaisis tän maan ja uusi aika koittaa”

Idols finalists, Finland 2003

The year 2025 is drifting towards its close. It is shaping up to be an excellent year for European equities, while for US equities, measured in euros, the year has been rather modest for investors.

The investment year 2025 could be described as geopolitical fumbling, where the biggest topics of discussion were artificial intelligence, AI-driven energy companies and the defence industry. Investors seemed to be chasing themes as if there were no tomorrow, which has not been at all unusual over the past five years. Large caps have continued to draw the longer straw compared with small caps.

In 2024, we wrote a market letter comparing the market environment at the time to the 1990s. I would say that the 1990s still remain the best analogy, even if not a perfect one. That market letter can be read here.

In short: in the 1990s, large caps dominated because their earnings growth was as good as, or even better than, that of small caps. At the same time, investor enthusiasm for new technological innovations was extremely high. The 1990s were a lost decade for small-cap investors, before the situation reversed completely in the early 2000s. More on the small-cap theme later.

Another clear point of comparison with the 1990s is the pursuit of innovation-related narratives. AI investments are reaching almost epic proportions, as the largest US companies pour money into AI infrastructure.

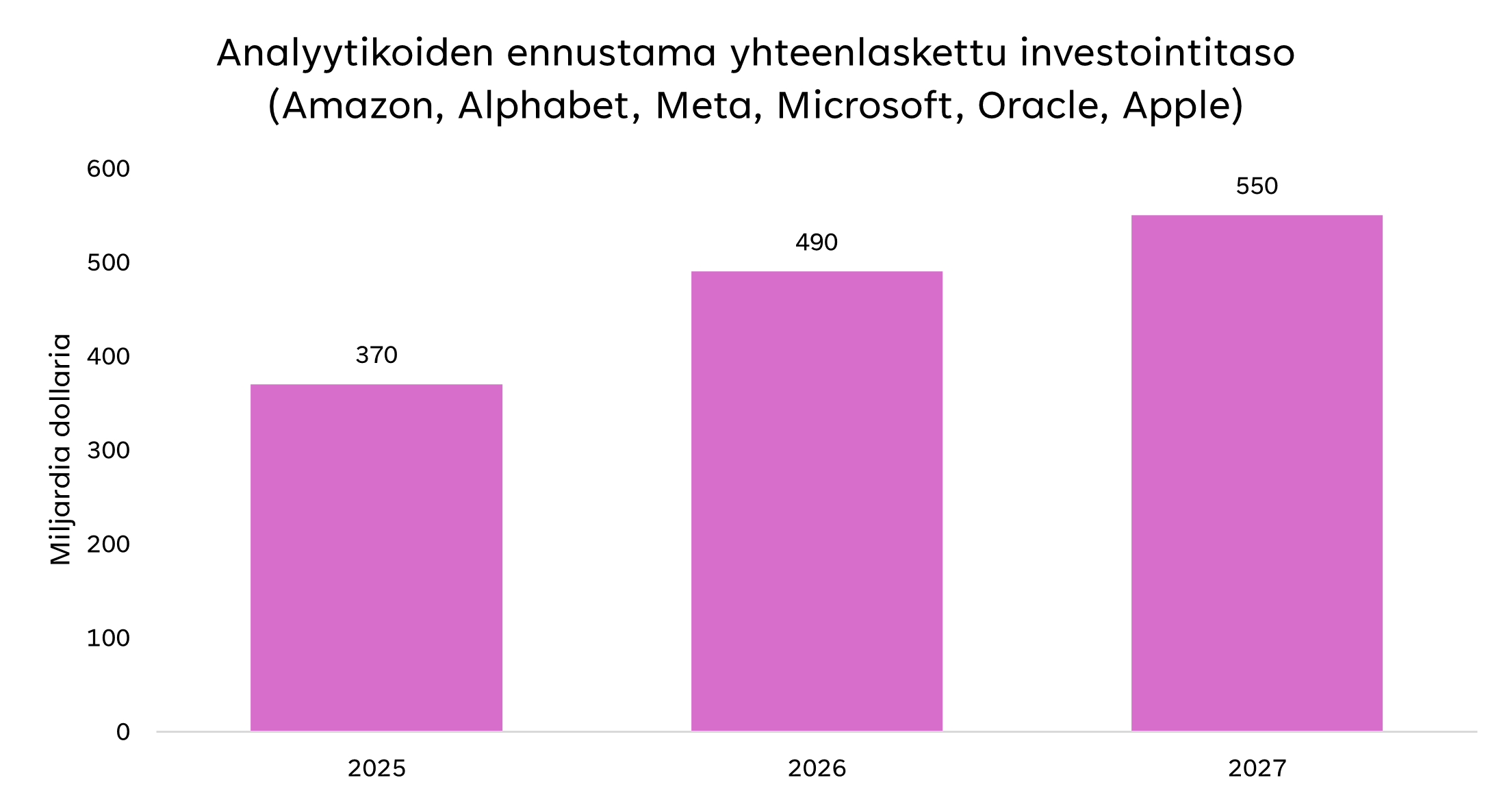

Figure 1: AI/data centre investments by the largest investors in the United States

Source: Proprius Partners, FactSet

The combined amount over three years is USD 1.4 trillion. Depending on the calculation method and assumptions used, this corresponds to approximately 40% of the total capital expenditure of S&P 500 companies. That sounds large, but it is fairly consistent with the fact that these companies account for around 30% of the total market capitalisation of the S&P 500 Index.

As for Europe, let us look a little more closely at what actually happened in the region’s equity markets.

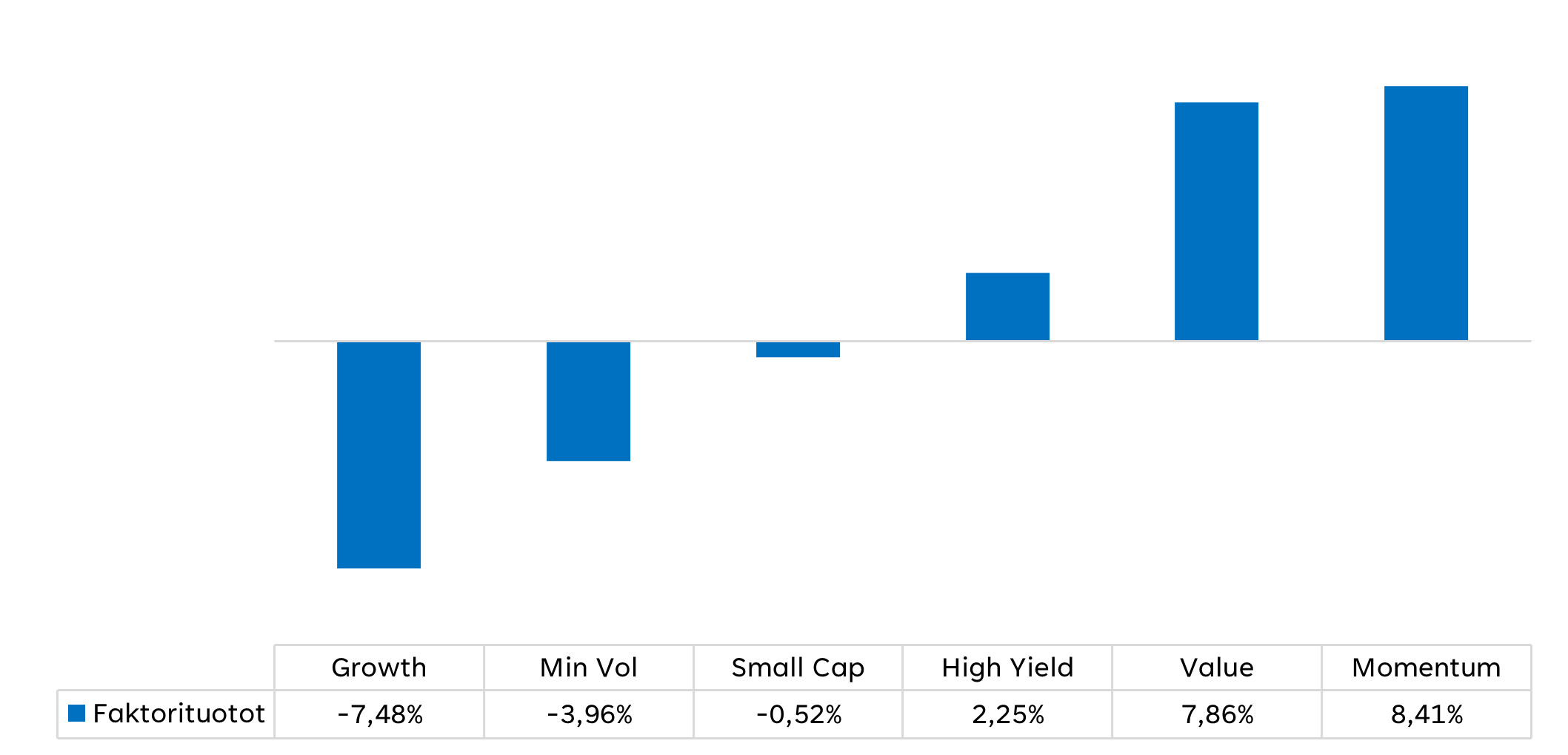

Figure 2: Factor outperformance and underperformance in European equity markets

Source: Bloomberg, Proprius Partners

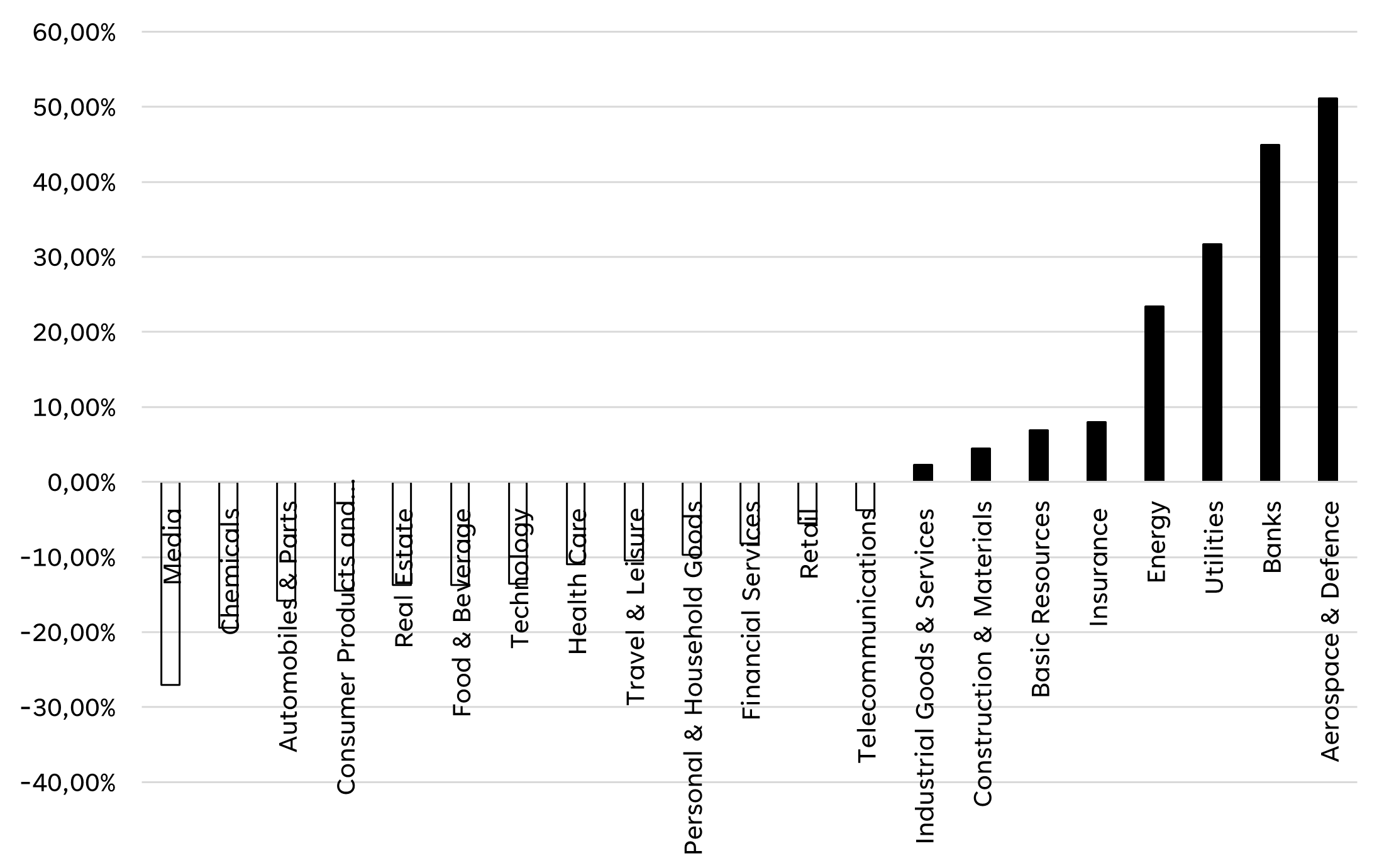

Figure 3: Sector returns in European equity markets

Source: Bloomberg, Proprius Partners

As the charts above show, Europe’s year can be summarised through a few key themes:

- The renaissance of the defence industry as a result of a shift in security policy. This has been most visible in German defence companies, but also in Finland, for example in Bittium.

- A year of strong performance for banks. The relative rally that began with the normalisation of interest rates gained further momentum this year. This was visible quite broadly across bank stocks and, in Finland, particularly in Nordea’s share price performance.

- Energy and utilities received a clear boost. This reflects a combination of bottleneck thinking around AI infrastructure and Europe’s strategic priorities. Energy self-sufficiency and energy investments have become increasingly important themes, and political pressure suggests that the theme is likely to continue developing relatively favourably in the future. There are several beneficiaries, but particularly notable examples include high-voltage cable manufacturer Prysmian and Siemens Energy, supported by both the restructuring of the Gamesa division and the substantial market opportunity in turbine projects aimed at balancing electricity generation. In Finland, the development was reflected in companies such as Fortum and Wärtsilä.

For active portfolio managers, the year has admittedly been painful. Few active funds have had significant weights in banks, energy companies or even utilities. Companies in these sectors do not typically meet the criteria of long-term investors. The biggest blind spot for active funds has been the defence industry, as ESG policies prevented investments in the sector, and, in addition, the entire industry had been practically dead in Europe for almost 30 years.

Forward We Go, Said Grandma in the Snow

Most 2026 outlooks published by major investment banks — Goldman Sachs, J.P. Morgan, Morgan Stanley, Deutsche Bank and BofA — forecast that equities will continue to rise. The backdrop remains a relatively strong economy, easing inflation and expectations of lower interest rates. This is a classic bull-market setup: reasonably strong fundamentals combined with market appetite for risk. Still, much of this is already priced into many markets.

The US equity market still appears to be the engine of global markets. AI investments are, in practice, the backbone of US economic growth. Europe is seen more as a value investor’s region, where growth is generated more selectively.

European equities remain clearly cheaper than US equities. This is no coincidence: the European economy grows more moderately, and exchange rates — particularly the strong euro — reduce the earnings of many export-oriented companies.

Despite this, banks are still not particularly expensive. Earnings profiles are improving as the yield curve and economic activity develop, but negative economic news could halt this thematic rally.

Many cyclical sectors, such as industrials and consumer cyclicals, can also perform well if the economy does not surprise negatively.

High-quality but forgotten companies, particularly in healthcare and strong consumer brands, may offer earnings growth and protection against consensus expectations. Healthcare has been under pressure for a long time.

Export-driven sectors such as autos and chemicals may remain weak if the euro stays strong and cracks appear in global demand. In addition, the automotive and chemicals industries face structural headwinds, which is why we generally seek to avoid them.

In the United States, AI investments support earnings growth, and long-term total returns are heavily dependent on corporate investment. Mega-cap technology companies are expensive, but not yet explosively overvalued, provided growth continues. The risk, however, is that the rally becomes too narrow: if the winners become concentrated in an even smaller group, market sensitivity to volatility increases.

Small Caps – Will 2026 Bring Another Beating?

Small caps have spent the past few years in the corner of the market — and not without reason. Rising interest rates, higher financing costs and an uncertain economic environment have hit smaller companies harder than larger ones. Now, however, the situation is starting to change, even if the headlines are not yet shouting about it. The structural headwind is easing.

First, small caps are interest-rate sensitive. Their cash flows are more uneven and their access to capital markets is narrower. When interest rates rise, this is immediately reflected in valuations and earnings expectations.

In 2026, the situation already looks somewhat different. Lower rates do not automatically make small caps winners, but they do remove one key structural burden. That alone is enough to change the nature of the game.

In addition, one difference is clear: Europe looks more interesting than the United States.

European small caps are:

- less dependent on global capital flows

- more often driven by domestic markets

- still valued at clearly lower levels relative to large caps

In the United States, small caps do benefit from lower rates, but they are also more exposed to fluctuations in consumption and the labour market. In Europe, the story is more one of quiet normalisation than a cyclical explosion.

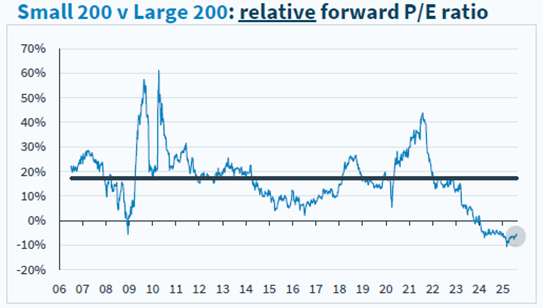

Small caps remain historically exceptionally cheap relative to large caps. This does not in itself trigger a rally, but it creates a setup in which bad news is largely priced in — and good news is not.

Figure 4: Relative valuation of European small caps compared with large caps

Source: Kepler Cheuvreux

This is a classic asymmetric situation:

- there is ground beneath the feet, meaning that devastating relative declines are less likely from here

- upside potential requires only small improvements

However, a word of warning is warranted: an aggressive rally in the small-cap index is unlikely. The “everything goes up” environment of the 2010s is not coming back.

The winners will be found among:

- profitable companies

- moderately leveraged companies

- companies with pricing power

- often niche operators

To throw some spaghetti at the wall, so to speak, and discuss the themes more specifically, the aim is to look for areas with relatively little hype and a surprising amount of realism:

- industrial specialists: components, automation, niche bits and pieces

- subcontractors to the AI ecosystem, not direct AI stories

- niche healthcare services

- niche defence companies

- local infrastructure and service companies

2026 may not necessarily be a celebration for small caps. It may, however, be the first year in a long time when they are no longer facing a structural headwind. That alone is enough to change the investment setup.

In small caps, patience, a focus on fundamentals and active portfolio management are not optional — they are prerequisites.

Then again, this is what we have been muttering for almost three years now. Perhaps even a broken clock is right once a day…

Proprius Portfolio Management: Top of Mind for 2026

As we leave 2025 behind and approach 2026, we want to highlight a few themes and sectors that we are watching particularly closely from our own perspective.

Defence

Our Uusi Eurooppa fund, in which defence and aerospace are one of the four key themes, was launched in May 2025. By then, the largest moves in defence had already taken place, and in the short term it was not realistic to expect the shares to continue rising aggressively. However, from our perspective, the longer-term rise in defence company share prices is relatively well justified. Following the recent correction, reasonably attractive buying opportunities have emerged in these companies.

This logic is based on a few key views:

- The renaissance of the defence industry is not dependent on the war in Ukraine. It is linked more broadly to the changed geopolitical environment. The cold war between China and the United States is driving this trend, and the broad range of related threats has forced a rethink of defence, particularly in Europe. In this context, German defence investments stand out, as Germany is one of the few European countries with the financial capacity to increase spending significantly from previous levels.

- Defence company valuations are not unreasonable when one considers earnings growth over the next five years and beyond. In many companies, the PEG ratio — the P/E ratio divided by earnings growth — is approaching 1. In practice, this means, for example, that if the P/E ratio is 30 and next year’s earnings growth is 30%, the PEG ratio is 1, which can be considered inexpensive.

- To continue the previous point: strong earnings growth over several years explains why these companies should not be valued in the same category as traditional industrial companies — nor in line with their own historical valuations.

The share prices of these companies will be volatile, as few investors hold companies in this category as strategic long-term positions. They are often seen as tactical views and as attempts to chase share price momentum. For many active portfolio managers, holding these companies in portfolios remains uncomfortable, regardless of how ESG policies evolve.

In our view, the operational success of these companies over the long term is quite evident — and at the same time unfortunate from the perspective of the world. This is the environment in which we now live and will continue to live. Following the logic of the Cold War, the most likely outcome is that one of the competing powers eventually collapses.

Small Caps in German-Speaking Europe

Among Proprius funds, DACH Value performed excellently this year. The median market capitalisation of the fund’s portfolio companies is just under EUR 4 billion. One might naturally assume that the fund’s success came from strong performance in companies of this size, but that is not the case.

The fund has managed to navigate exceptionally well against the continued weakness of smaller companies. Large caps and the defence industry have accounted for a significant share of the 2025 return, while smaller companies have provided practically no support at all. If the small-cap environment improves even slightly in 2026 — as we have argued in this letter — the fund should have reasonable conditions to succeed next year as well.

Additional support comes from Germany’s fiscal package and a generally improved sense of momentum in the region. We have written more about this previously; that letter can be read here.

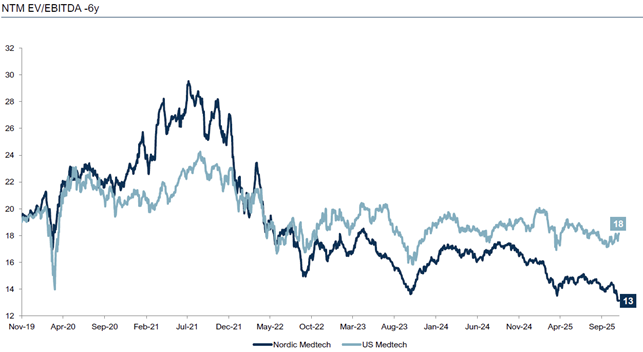

Healthcare – Dust Bunnies Rolling Around, and Nobody Cares

Within Proprius portfolio management, we have discussed the healthcare theme throughout the year. Almost all of our funds are connected to the theme in one way or another. The largest exposure is found in the Micro Scandinavia fund, although through micro-cap companies.

The healthcare sector, particularly the equipment and technology segments, has been in very poor shape for a long time. The post-COVID hangover, budget pressures among end customers, geopolitical uncertainty and weakness in the Chinese economy have created significant headwinds in recent years. Positive catalysts have been scarce.

Another key reason for the sector’s weak development is simple: money has moved elsewhere. The sector’s own challenges, combined with the opportunity cost of not being invested in technology and other dominant themes, have been too much for investors. Despite this, it is worth remembering that population ageing is not going away and will continue to act as a fairly resilient growth driver for the sector and its subsectors. Many healthcare markets are still growing at annual rates of 10–15%, and much more steadily than technology-driven markets.

We believe 2026 could be an interesting year for these companies. They are not as strongly linked to global economic growth, but partly live a life of their own. Valuations have normalised since 2021, and investor attention has been away from the sector for a long time. Opportunities can be found here for those willing to take considered risk.

Figure 5: Development of valuations in the Nordic health technology sector versus the US health technology sector over the past six years

Source: Pareto, FactSet

Will Consumer Demand Recover, or Will Money Remain Sitting in Bank Accounts?

Consumer demand has been weak, particularly in 2025. This has been clearly visible in domestically oriented companies on the Helsinki Stock Exchange, but also more broadly across Europe. Consumer products and services were among the weakest-performing sectors in 2025. The same applies to luxury goods companies, whose long supercycle came to an abrupt end as Chinese demand faded.

As a result of these trends, many consumer companies have been repriced sharply lower. Valuations are low in places, and the current situation does not appear sustainable. Even small pieces of positive news can therefore trigger large share price moves. A good example from Finland is Verkkokauppa.com, whose share price fell so low that even a small positive signal led to a significant rally.

Final Remarks

Let us summarise this long text:

- 2025 was driven by themes and large caps

European equities performed well, while the United States delivered more modest returns measured in euros. The market was dominated by narrow themes, particularly AI, energy and defence. Large caps once again outperformed small caps by a wide margin. - In Europe, a few sectors delivered most of the returns.

Defence, banks, and energy and utilities accounted for most of the European market’s return. This made the year challenging for active portfolio managers, who typically did not have large weights in these sectors, especially defence due to ESG restrictions. - Looking to 2026: US growth, European selectivity

Markets expect equities to continue rising as interest rates fall, but much of the positive backdrop is already priced in. The United States remains the engine of markets, driven by AI investments, while in Europe returns will increasingly come from selective stock picking rather than from the index level. For euro-based investors, however, it is worth being somewhat cautious about the US dollar. - The headwind for small caps is easing, but no miracle is expected

Small caps are historically cheap relative to large caps. Lower rates remove a key structural burden, but a broad small-cap rally is not expected. The winners will be found through active portfolio management among profitable niche companies with pricing power. - The sector and theme focus for 2026 is selective

Proprius’ interest is directed towards the defence industry, undervalued niche segments in healthcare, the consumer sector where even small signs of demand recovery can have a strong impact, and German small caps supported by structural investments and an improving operating environment.

That is where we stand. We are satisfied with the portfolio company selections in Proprius’ funds as we enter 2026. Many of the funds can perform well through earnings growth alone, provided forecasts are even close to being met. In addition, even a small ray of sunshine in the small-cap wasteland would create significant upside potential.

Thank you to all our readers and clients for this year. See you next year!

“Good morning, and in case I don’t see ya, good afternoon, good evening, and good night!”

Truman, Truman Show 1998

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa