Looking for a winner

When managing an investment portfolio, decision-making always consists of two parts: the allocation decision and the instrument selection.

The allocation decision determines which asset class and market should receive the next allocation of capital. Instrument selection, in turn, is the decision on what kind of instrument or strategy should be used to gain exposure to that asset class and market.

If you are managing your investment portfolio with a 10-year horizon, both the allocation decision and the instrument selection currently support investing in the DACH Value fund. I will next argue why the DACH Value fund could be the most interesting long-term investment opportunity in your portfolio.

“Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years.”

Warren Buffett

My argument rests on two key factors: the long-term return expectations of German mid-cap companies, and our portfolio managers’ decades of experience and proven ability to find investment opportunities in the region that outperform the broader market. Let us dig a little deeper.

Long-Term Return Expectations – Why Do They Matter?

A year ago, many experienced investors allowed FOMO — Fear of Missing Out — to guide their decisions and shifted capital from Europe to the United States precisely when they should have done the opposite. If you had read and believed the blog I wrote exactly one year ago, your portfolio would most likely have performed better.

My intention, however, was not to give one-year investment tips, but to help investors succeed over the next decade. After all, no one could have predicted — least of all me — how Trump’s trade policy would affect the dollar. This year’s events have nevertheless once again served as a reminder of how studying long-term return expectations can improve your probability of success as an investor. This text is therefore about the most likely winner over the next 10 years, not over the next year.

Figure 1. Returns of the S&P 500, STOXX 600 and the Helsinki Stock Exchange since the publication of “This Time Is Different… Again”.

Source: Bloomberg, Proprius Partners.

Investors who shifted capital to the United States have not been entirely wrong about the strong performance of the local equity market. The weakening of the dollar has, however, eaten away around 9 percentage points of the returns shown above, meaning that the return gap versus Europe in local currency is more moderate.

Where these investors have been wrong is in underestimating Europe’s potential. When starting from the bottom, not much is needed to generate good returns.

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach.”

Peter Lynch

Why Is Europe Interesting Now?

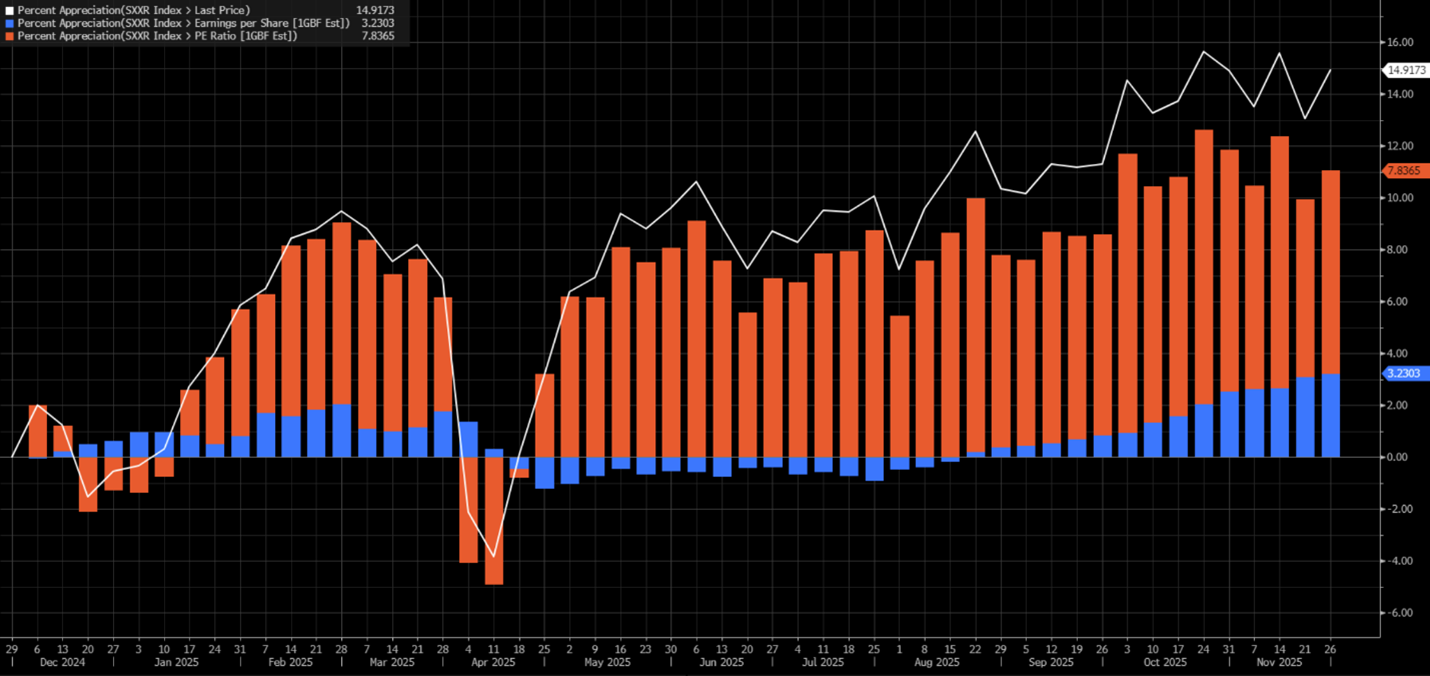

As noted in my blog a year ago, starting valuation provides the best explanatory power for long-term returns. This year, it has also explained short-term returns. The positive development of the STOXX 600 equity index, which represents European large caps, has this year been explained almost entirely by the normalisation of valuation multiples.

Figure 2. STOXX 600 return between 26 November 2024 and 26 November 2025, split into earnings growth (blue) and change in valuation multiple (orange).

Source: Bloomberg, Proprius Partners.

Last autumn, markets had priced a great deal of pessimism into European equities. Now that cautiously positive news has started to emerge from the European economy, valuation multiples have begun to normalise rapidly. Although the European economy still faces challenges, what matters for investors is the direction of change — and that direction is now upwards.

Europe is therefore no longer cheap. Valuations have returned to a long-term neutral level, but Europe remains cheaper than most of the rest of the world. Whereas Europe’s higher long-term return expectations were previously explained purely by low valuation levels, the most significant change in research houses’ reports this year has been the long-term earnings growth forecasts for Europe.

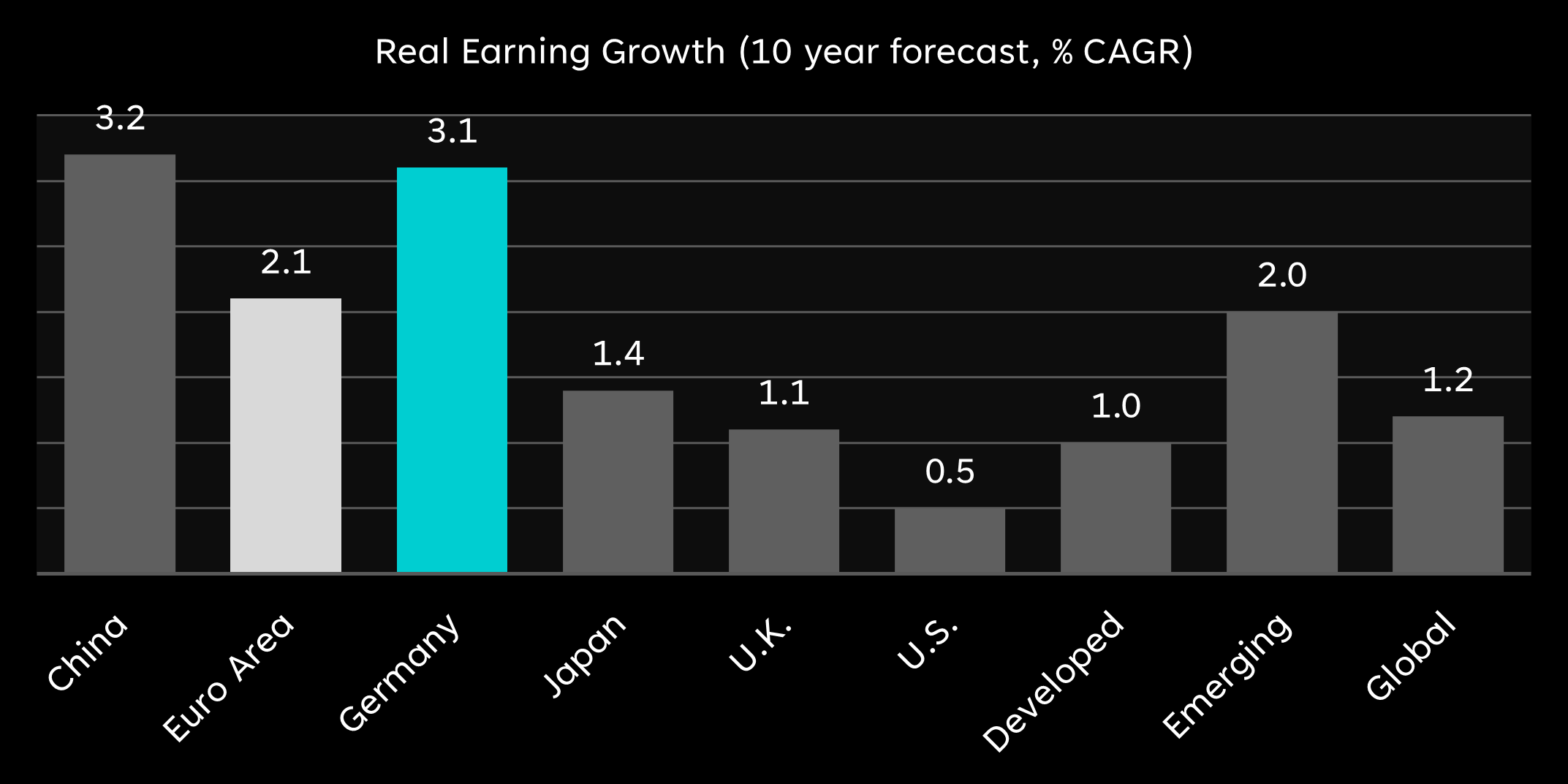

At the same time as global earnings growth is expected to slow over a 10-year horizon, Europe — and Germany in particular — is expected to deliver respectable earnings growth.

Figure 3. Real earnings growth forecasts (nominal growth minus inflation) for the next 10 years.

Source: MRB Partners, The Perils Of Extrapolation, 11/2025.

The expected improvement in European earnings growth is often justified by the easing of austerity that began with the euro crisis, affecting consumers, the private sector and governments alike. Among European governments, Germany is in reality the only country with significant room to increase debt.

Germany’s fiscal policy activism is therefore seen as the most interesting development in Europe in decades. Many have bet on US AI dominance on the assumption that it will increase US productivity and ultimately corporate earnings growth. MRB, however, offers an interesting angle to the AI discussion in its report, commenting that it expects higher productivity to push up real interest rates, which would crowd out the positive impact of productivity growth on corporate earnings.

Few analyses I have seen are quite this pessimistic about US earnings growth. Still, current US valuations continue to be seen as the greatest challenge to strong long-term returns.

In Europe, by contrast, improved earnings growth prospects combined with current valuations once again place the old continent near the top of the long-term return expectations of almost all international research houses.

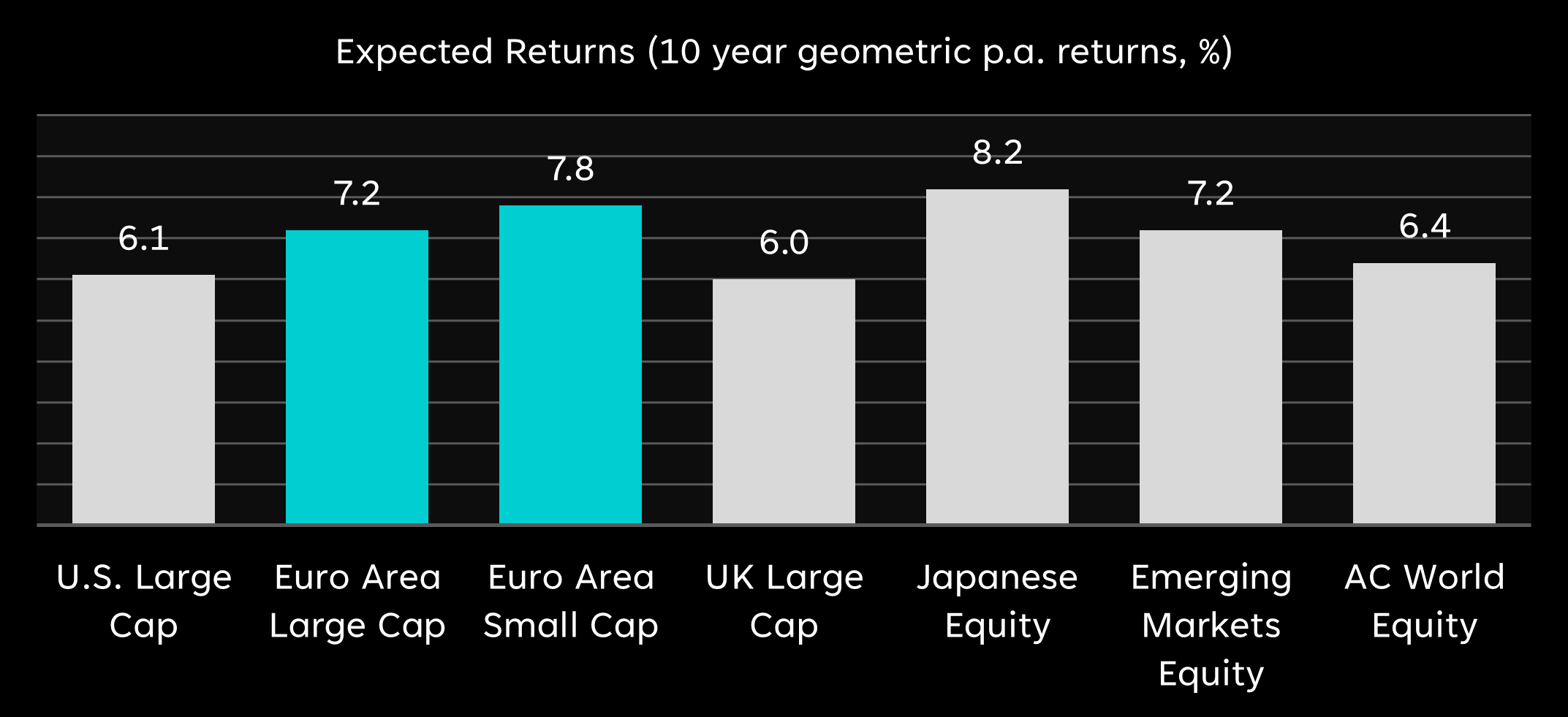

Figure 4. 10-year return expectations for different equity markets.

Source: J.P. Morgan Asset Management, 2025 Long-Term Capital Market Assumptions.

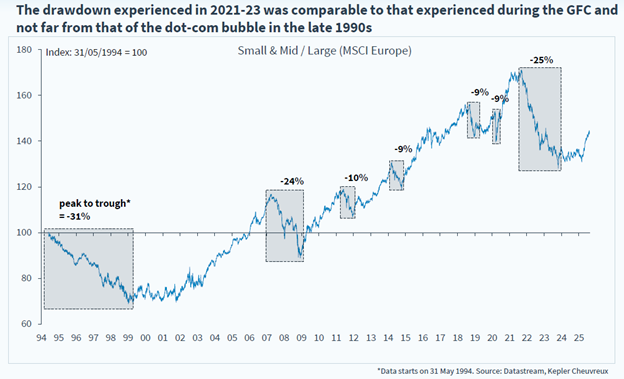

The expected return of small caps is worth noting. As a rule, the smaller the company, the weaker its performance has been since 2021. As a result, valuations in small caps are at historically low levels, and the size premium is widely available in the market.

The small-cap turn has, of course, been expected for a long time, and in this riskier part of the market the wait can sometimes feel very long indeed. If the investment horizon is 10 years, however, the key issue is not timing the turn — which will almost certainly be wrong — but knowing that one is buying from somewhere other than the top.

Figure 5. Relative performance of small and mid-sized European companies compared with large European companies.

Source: Kepler Cheuvreux, Goldilocks or a Summer Mirage?, 8/2025.

To summarise the Capital Market Assumption reports I have waded through this autumn: the fundamentals still look far from foolish for the European equity market, and all roads lead to German mid-sized companies.

Europe’s Engine Is Starting

This year, Europe has woken from its slumber of relying on great-power politics and has started taking action to survive — largely out of necessity. Draghi’s report from last year has been pulled out of the drawer, and suddenly its content has begun to attract wider interest across Europe.

Despite this positive movement, it is worth remembering that no one would be surprised if the end result were once again a collection of fine speeches and reports with no concrete action. Europe is highly fragmented, which makes finding a common objective difficult.

Fortunately, it does not really matter whether Europe collectively manages to achieve anything. What matters most is whether Europe’s largest economy, Germany, does. Europe’s future now rests heavily on Germany.

In 2025, Germany made a historic U-turn in its economic policy: the country’s parliament approved an estimated EUR 1,000 billion investment package targeting infrastructure, defence, digitalisation and the green transition. The debt brake was loosened, enabling growth across Europe.

At the same time, within a very short period, Merz pushed through the Investment Immediate Programme Act, under which corporate tax will fall from 2028 onwards. Before that, the law will stimulate the economy through EUR 46 billion in tax incentives during 2025–2029, benefiting to a large extent precisely the medium-sized, capital-intensive companies making investments.

In the background, the Growth Opportunities Act is also in motion, containing tax reforms that encourage investment and reduce bureaucracy, while the European Chips Act strengthens Europe’s semiconductor ecosystem by improving research and production within the EU and reducing external dependence.

The private sector has also joined the effort. Under the “Made for Germany” initiative, companies have already committed to investing EUR 735 billion in Germany in exchange for the implementation of reforms, such as less bureaucracy, a better energy and tax framework, and faster permitting processes.

Although Germany is a politically polarised country — as all countries seem to be these days — it can be said that Merz has truly got things moving during his short tenure. Of course, one can always raise critical points about expansionary fiscal policy. There is no benefit to taking on more debt if the money flows unproductively into maintaining the welfare state.

Fortunately, with the current composition of the German government, there is little risk that the money will go into social security or expanding public-sector bureaucracy. The aim is specifically to direct it towards investment.

The world and Germany’s challenges have changed since the era of Gerhard Schröder, but there are some similar winds of change in Merz’s approach to those seen in Schröder’s 2003 reforms, when he turned Europe’s sick man into Europe’s export powerhouse. The fruits of those measures were also harvested in the equity market in 2003–2008.

“Know what you own and know why you own it.”

Peter Lynch

The concrete impact of Merz’s measures on companies’ revenues, earnings and ultimately the economy will not be visible until late next year at the earliest. Equity markets have, of course, already partly reacted to the factors mentioned above.

Germany’s broad DAX index has delivered strong returns since the collapse of the previous government about a year ago, as international investors became excited about the opportunity created by this change.

This, however, illustrates the simplicity of today’s capital allocation. Index investors have been buying the German broad index hand over fist — in practice Germany’s largest companies — without really considering where this expansionary fiscal policy will ultimately flow.

Many obvious basic materials and construction industry companies, such as Heidelberg Materials AG and Hochtief AG, have also enjoyed investor attention. Their revenues will likely benefit from state-commissioned infrastructure projects, and on this we agree with the market. However, these companies represent lower value-added business models and are therefore not particularly interesting over the long run.

Instead of Germany’s largest companies and the most obvious beneficiaries of the stimulus package, we are interested in higher value-added companies in Germany’s mid-cap universe. Figuratively speaking: if stock picking were simply about staring at the first derivative, making money would be very easy. Investors often forget that the second and third derivatives are more important.

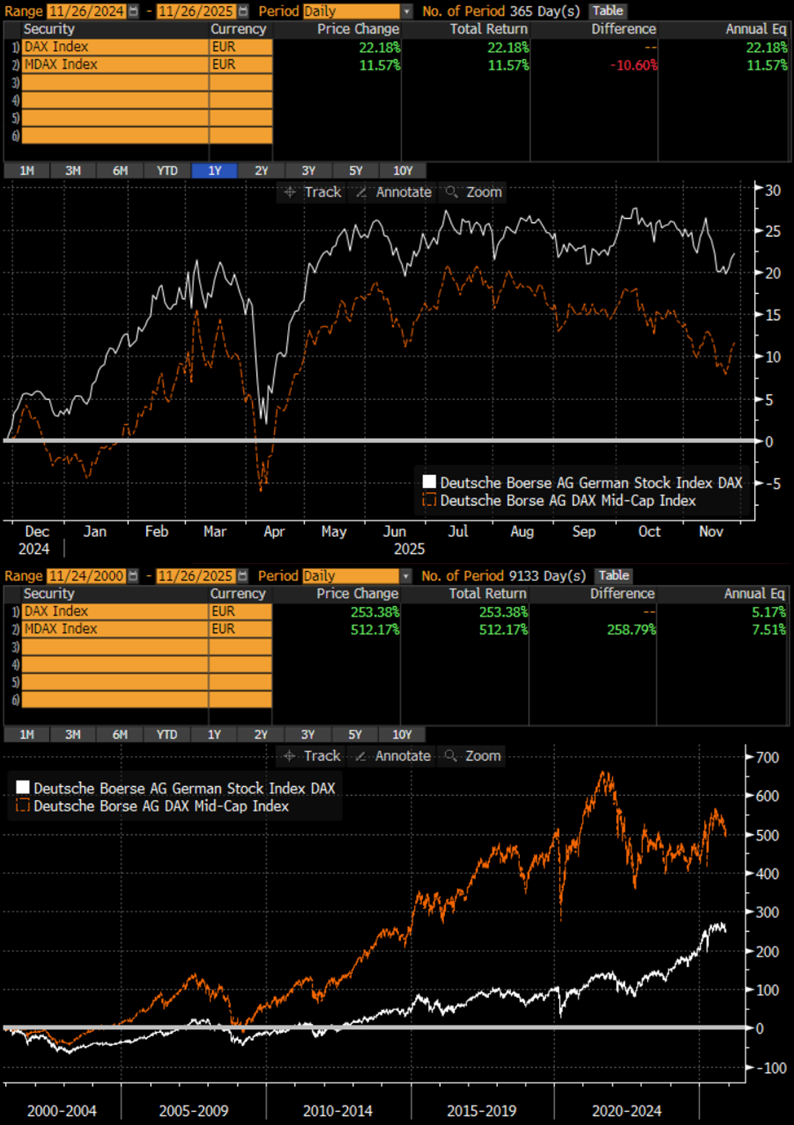

Figure 6. DAX (white) vs. MDAX (orange), representing mid-sized companies, over 1 year and 25 years.

Source: Bloomberg, Proprius Partners.

A distinctive feature of the German economy is the Mittelstand — a broad group of mid-sized, often family-owned companies. These companies make up the lion’s share of German businesses, employ 60% of the workforce and generate more than half of the country’s GDP.

Mittelstand companies are known for their long-term orientation, innovation and strong regional commitment. These are companies whose revenues are largely generated in Germany or the German-speaking European region, and which are therefore particularly well positioned to benefit from Germany’s expansionary fiscal policy.

Among Mittelstand companies there are a vast number of businesses unknown to many investors, yet whose market position in their own field is among the top three globally. Nowhere else in the world is there a comparable volume of little-known, strong niche companies.

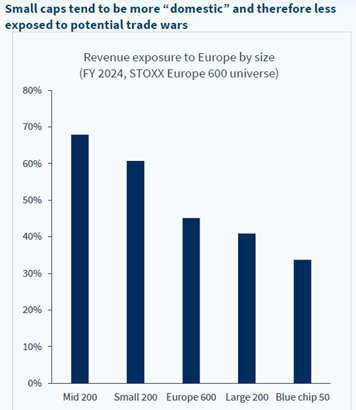

Figure 7. Revenue exposure to Europe by company size.

Source: Kepler Cheuvreux, Goldilocks or a Summer Mirage?, 8/2025.

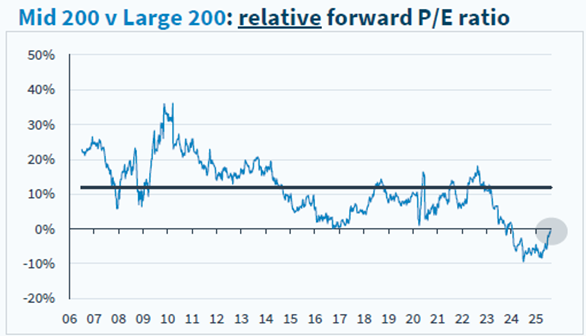

And best of all, these companies are typically completely overlooked by international investors and have therefore not yet received their share of the normalisation in valuation multiples. At the same time, they have suffered from the small-cap pain that began with the rise in financing costs in 2021.

Figure 8. Valuation of European mid-sized companies relative to large European companies.

Source: Kepler Cheuvreux, Goldilocks or a Summer Mirage?, 8/2025.

DACH Value – An Investment in the Heart of Europe

The DACH Value fund invests in companies in German-speaking Europe: Germany, Switzerland and Austria. The fund invests in companies of all sizes, but historically the highest-quality investment opportunities have been found specifically in the German mid-cap universe.

The fund is therefore particularly weighted towards this company segment, with German companies currently accounting for 67% of the portfolio and the median market capitalisation at EUR 3.7 billion.

The fund’s strategy is strongly rooted in the philosophy of value investing, without forgetting business quality. As a result, the fund’s median valuation is typically 10–20% below the market, while quality — measured for example by return on equity — is better.

At the time of writing, for example, the median 2026 P/E is 12.5 and EV/EBIT is 11.2. At the same time, the median ROE for this year is 16%. These are not bad figures at all for generating returns. The corresponding market figures are P/E 14.3, EV/EBIT 13.0 and ROE 14%.

It can therefore be said that our portfolio managers are operating in a company universe that is optimal from the perspective of long-term return expectations. But that is only one side of the story.

The more interesting side is the portfolio management team’s ability to find investment opportunities that outperform the market. Past performance is no guarantee of future returns, but if one needs to assess whether a portfolio manager has the ability to generate outperformance, historical returns relative to the market are often the only hard fact available.

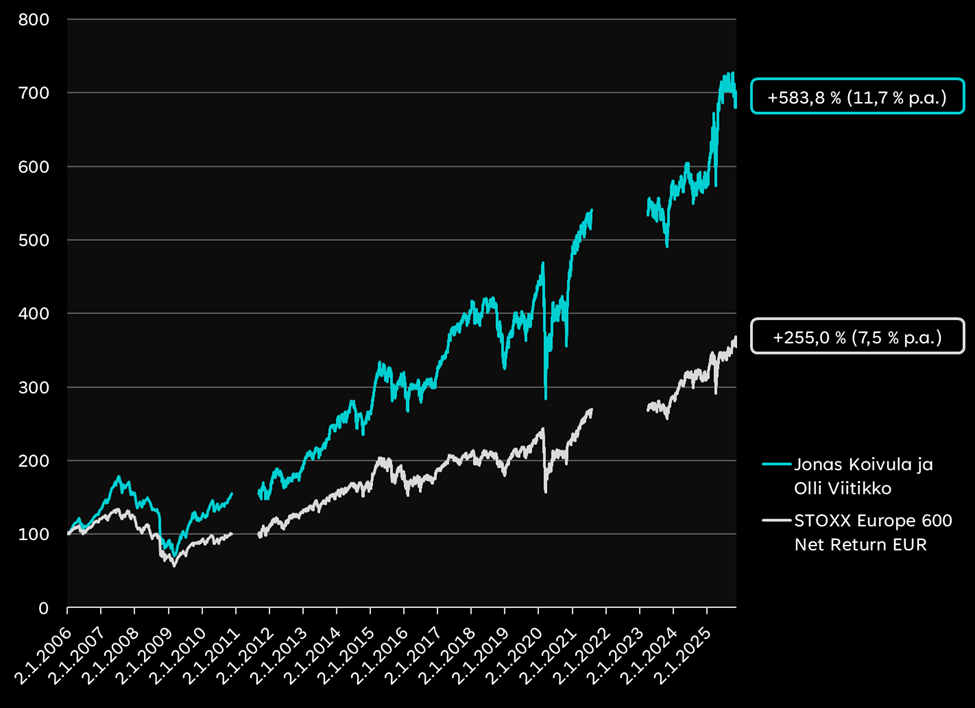

The fund’s portfolio managers, Jonas Koivula and Olli Viitikko, have over their careers generated average annual outperformance of 4.2% relative to the market through a value strategy investing in German-speaking Europe. Net of all fees. The history of this strategy goes back to 2006 and Fourton Fund Management, after which it continued at Taaleri, Aktia and now Proprius Partners.

Figure 9. Return history of the value strategy investing in German-speaking Europe and the STOXX Europe 600 Net Return EUR Index used as the reference return. Period: 2 January 2006 – 21 November 2025.

Source: Bloomberg, Proprius Partners.

What is this outperformance based on?

Focus and legwork.

Jonas and Olli have followed companies in the region for a combined 35 years, met company management teams, visited production facilities and built a deep understanding of their investment universe. It also helps that this market is not particularly efficient.

Germany has a weak equity investing culture, and historically both households and especially local institutions and pension funds have been conspicuous by their absence from the market. As a result, the German market is heavily dependent on international investors, which leads to a volatile market where investors are more interested in index-level figures than in individual companies.

This kind of environment is, first, excellent for a value investor who can take advantage of valuation overshoots caused by index movements, and more generally for high-conviction stock picking, because there are fewer pairs of eyes looking under the bonnet of the market.

“While some might mistakenly consider value investing a mechanical tool for identifying bargains, it is actually a comprehensive investment philosophy.”

Seth Klarman

The Winner Has Been Found

Long-term return expectations do not provide certainty, but they offer the best guidance available. They point the allocation decision towards investing in German mid-cap equities.

The characteristics of this market, its inefficiency and the fiscal policy shift offer outperformance potential through active portfolio management that is available in very few markets.

When we know that there is also a solution where the portfolio managers have decades of evidence of successfully exploiting this potential in that specific market, the appropriate instrument selection is the high-conviction DACH Value non-UCITS fund.

What the market return plus outperformance from this investment decision will ultimately be in 10 years is impossible to say — and we are not even allowed to guess. But I repeat my original claim: an investment made today in the DACH Value fund could be the most interesting investment opportunity in your portfolio over the next 10 years.

To close, I want to remind you that despite my strong view, no sensible person puts all their chips on even the most likely winner. As an investor, the goal is to operate like a casino. A casino can lose on any single spin, but if you keep the odds in your favour, success is guaranteed as the number of spins increases.

“It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.”

George Soros

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa