This Time Is Different… Again.

Long-term investors should, for once, believe in long-term expected returns based on academic research and, on that basis, avoid allocating capital to the US equity market — or at least to the S&P 500 Index — right now. Readers should, however, note that Proprius Partners does not have a fund investing in the United States, and my view can therefore be considered biased. If you dislike a barber recommending a haircut, or an asset manager challenging your current investment thesis, I recommend you stop reading here.

Investors should be interested in what kind of risk premium they are being paid for the risks they take. Of course, an investor can also be risk-neutral, in which case they are only interested in the expected return of investments — although that, too, is closely linked to the risk premium available from different asset classes. Sounds fairly obvious, does it not? Perhaps even too obvious, which is why investors time and again end up inventing ever more creative justifications for the attractiveness of investments, despite their low risk premia or expected returns. “But this time everything is different…”

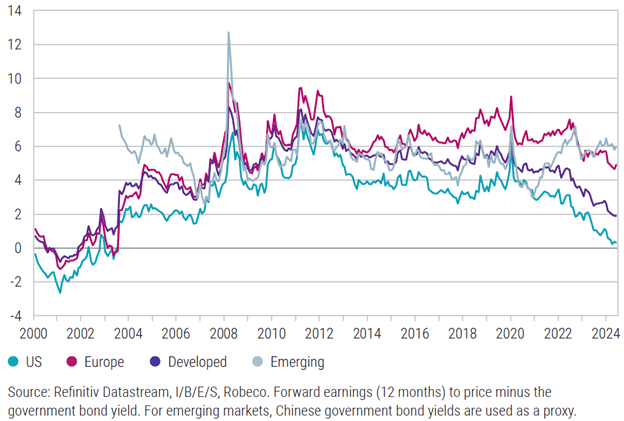

Figure 1: Equity risk premium across different equity regions

Source: Robeco

The US equity risk premium has fallen to zero. The last time it was at this level was in the aftermath of the dot-com bubble. In other words, the earnings yield of equities is now at the same level as the yield on the 10-year US Treasury bond, around 4.3%. At the current level of earnings growth, an investor has to believe in an endless rise in valuations in order to be rewarded for bearing equity risk. A long-horizon investor would be better off buying US government bonds.

Financial institutions calculate long-term expected returns for different asset classes and equity regions. Most of them publish these quite openly in their annual Capital Market Assumption papers. I went through the CMAs of eight different institutions: J.P. Morgan, BlackRock, Morgan Stanley, Invesco, Robeco, PIMCO, AQR and Goldman Sachs. Not a single paper had the expected annual return of the US equity market over the next 10 years higher than that of the global equity market, and in most papers the US had the lowest expected return among equity regions.

Of these institutions, Goldman Sachs caused a stir in the market in October by publishing its estimate that US equities are expected to deliver a nominal annual return of 3%, and a meagre 1% in real terms, over the next decade. Unlike one-year forecasts, which many institutions provide to their clients mainly to produce content, long-term expected returns have been shown to have at least some forecasting power.

So why do investors seem to ignore these expected return models and continue allocating increasing amounts of capital to the US equity market?

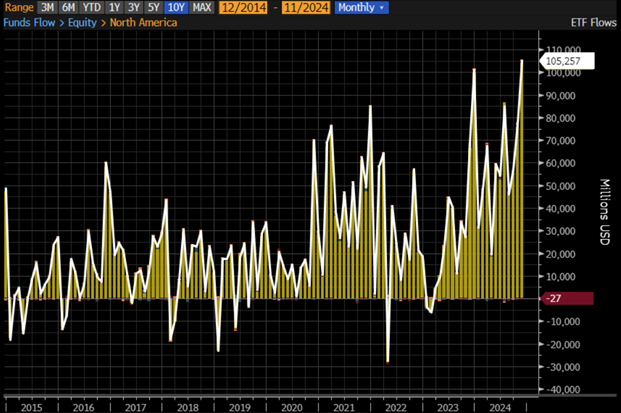

Figure 2: Net flows into US equity ETFs

Source: Bloomberg

Investors have a tendency to chase performance. The most important explanation for this irrational disregard of expected returns is the exceptionally strong multi-year performance of the US equity market and the resulting fear of missing out, or FOMO. As we know, similar situations have occurred many times in history, and they have rarely ended well. Thematic investing in the green transition in 2021 is one example of FOMO.

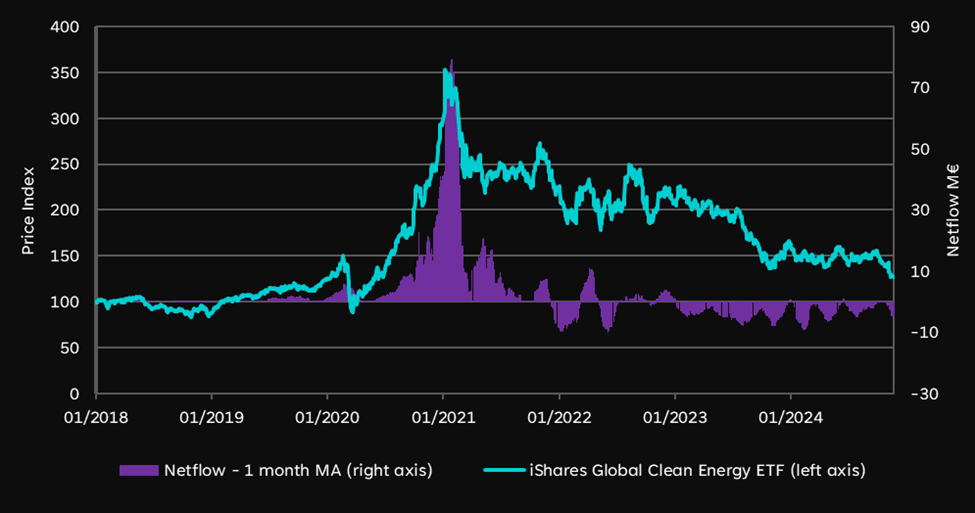

Figure 3: The green transition case

Source: Bloomberg, Proprius Partners

Investing after strong performance is a well-researched and recognised investment strategy known as momentum investing. As many studies show, however, momentum strategies typically work over a 6–12 month horizon. The typical investor, by contrast, assesses the future outlook of markets using the past 3–5 years and allocates capital to markets that have performed well over that period. From the perspective of generating returns, this is usually the worst time to start shifting portfolio allocation. As Cliff Asness of AQR, among others, reminds us, rather than following the trend over a 3–5 year horizon, moderate contrarian investing has been shown to be the better strategy.

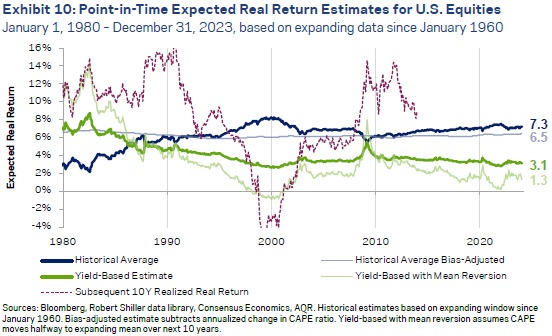

Figure 4: Expected 10-year real returns of US equities versus realised 10-year annual real returns

Source: AQR

As the chart above shows, if one had followed historical returns, US equities would have looked like the most attractive investment opportunity in 2000. In reality, that investment would have generated an average annual real return of -3% over the following 10 years. Forward-looking earnings yield-based metrics, by contrast, have provided better forecasts of future equity returns.

So far, investors who have allocated capital to the United States over the past three years can be very satisfied with their decision. Perhaps everything really is different this time, and expected returns do not tell the whole truth. But let us return to expected returns. What exactly do they include?

The risk premium is often closely linked to an asset class’s expected return, but it is not the whole story. Although long-horizon forecasts, roughly 10 years, involve significant uncertainty, they have considerably more forecasting power than short-horizon forecasts, where unpredictable macro factors play a major role. One example is the policy actions of the incoming US president, which are likely to affect equity returns in the short term, but whose importance diminishes over a longer horizon.

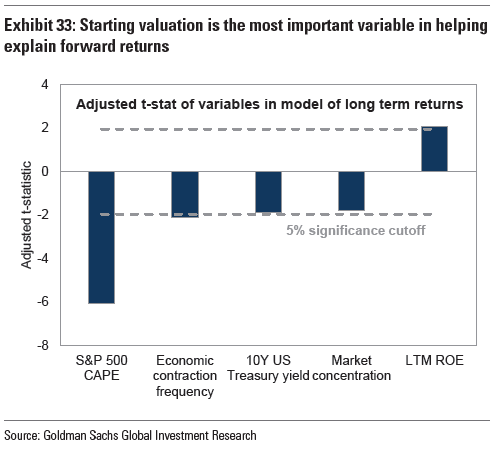

The same applies to equity valuations. In the short term, valuations can be almost anything, and therefore the starting valuation at the beginning of an investment period does not explain short-term equity returns. Over the long term, however, the starting valuation has been seen as the most significant explanatory factor for expected returns.

Figure 5: Explanatory power of different variables for expected returns

Source: Goldman Sachs

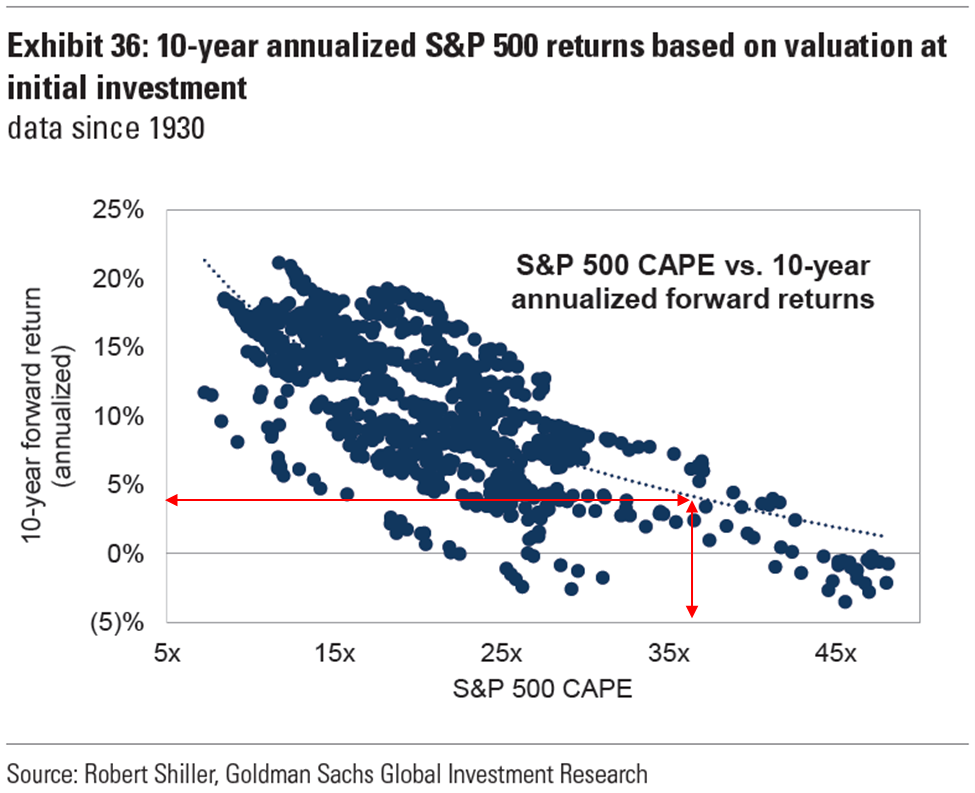

The recent strong performance of the S&P 500 Index has been largely driven by valuation expansion, and the index’s current valuation is therefore close to historical highs. By far the most widely used valuation metric in expected return models is Shiller’s CAPE, a cyclically adjusted P/E ratio where the current price of companies is divided by their average earnings over the past 10 years. The current CAPE of 38x corresponds to the 97th percentile of the metric since the 1930s and points to a future annual return of 4%.

Figure 6: Relationship between starting valuation and subsequent 10-year returns

Source: Goldman Sachs

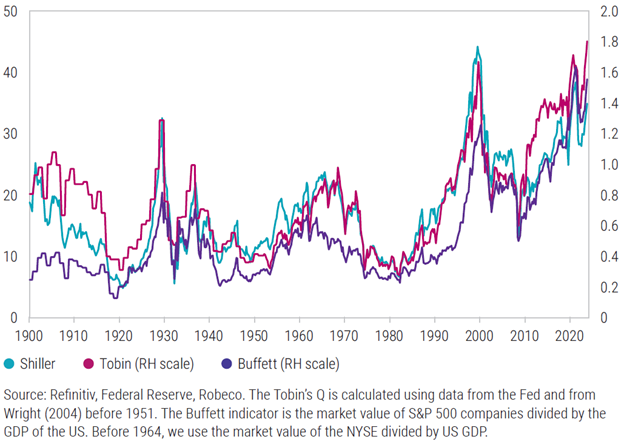

Whether one looks at the US equity market through CAPE or other valuation metrics, it is hovering close to all-time highs.

Figure 7: Valuation of the US equity market by different measures

Source: Robeco

Expected returns do, of course, include variables other than valuation. These variables vary somewhat between models, but for example, the current rush into the US market despite valuations is often justified by stronger economic growth than in Europe. Typically, higher economic growth forecasts are incorporated into models as terminal growth in corporate earnings. However, higher economic growth forecasts do not appear to be enough to make the United States a particularly attractive market, as all eight institutions mentioned earlier have included economic growth forecasts in their models and still arrived at lower expected returns for the US than for the global equity market.

At this point, I believe the reader is wondering whether the Mag 7 companies will be taken into account in this analysis at all. It is true that the high valuation of the US market is largely due to the Mag 7 companies, and therefore the situation changes in terms of expected returns if one invests in the US without them.

In fact, Goldman Sachs’ widely discussed expected return forecast was one of the more positive ones for the US equity market. Their model also included market concentration as one variable, and for that reason they also examined the US equity market through the S&P 500 Equal Weight Index, for which they assign a long-term expected return of 7% per annum instead of 3%. In the S&P 500 Equal Weight Index, all companies receive the same 0.2% weight regardless of size, and therefore the Mag 7 companies do not dominate it.

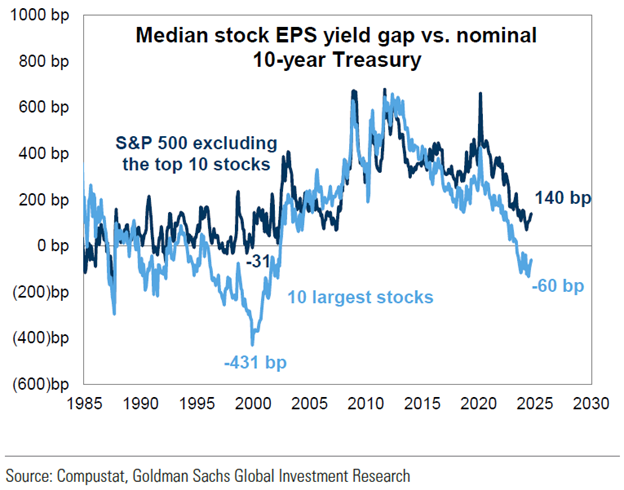

There is a significant difference in valuation, and therefore in equity risk premium, between the 10 largest companies and the remaining 490. High valuations are justified by the dominant market positions of the Mag 7 companies, which are expected to allow them to maintain strong growth numbers into eternity. Goldman Sachs nevertheless notes that statistically it is very difficult to maintain growth and margins over a decade. Once the slope of growth eventually moderates, the correction in valuation multiples is typically harsh.

Figure 8: Equity risk premium: S&P 500 top 10 vs. bottom 490

Source: Goldman Sachs

Agreeing with Goldman, it is quite reasonable to invest in the United States through the S&P 500 Equal Weight Index instead of the market cap-weighted S&P 500 Index, as this gives investors more exposure to small and mid-sized companies. Psychologically, however, the situation does not differ much from the investor’s Europe versus United States allocation dilemma. By investing in the equal weight index, you would still be heavily underweight the Mag 7 companies and would still suffer from FOMO — the original reason for moving to the United States. From the perspective of expected returns, however, the situation would be significantly better.

Expected returns therefore do not support investing in the US equity market, mainly due to current valuations. Of course, there is considerable uncertainty around the estimates. US valuations above historical levels are often justified by structural changes, such as lower corporate taxation. However, one can reasonably ask whether the hierarchy between asset classes should not remain intact over the long run regardless of the level of taxation. Equity risk should presumably offer some premium relative to the world’s best-known safe haven, although that safe haven does, of course, carry meaningful interest rate risk with an investment horizon of less than 10 years.

Why, then, allocate capital to the United States now? The United States is the most important equity market in the world. It represents 63.9% of the investable equity universe, and therefore from a portfolio theory perspective it is highly reasonable to have exposure to the US in a portfolio now and in the future. If, however, you have not invested in the US over the past 20 years, or you have been underweight that market, is now the time to start closing that gap? Based on the arguments presented in this text, among others, I would say no. Not from a tactical perspective, and not from a strategic perspective.

Of course, the issue immediately becomes more complicated when the concept of active risk, or tracking error, is brought into the discussion. Investors who manage other people’s money in particular are forced to consider this. As the legendary Yale endowment manager David Swensen described the principal-agent problem among institutions: “It is better to fail conventionally than succeed unconventionally.” That is why an investor can find reasons to shift capital, for example from Finland into the S&P 500 Index, even right now. In the long run, they will probably lose money on that trade, but they will lose alongside everyone else, and therefore keep their job. Unfortunately, investing in the S&P 500 Equal Weight Index keeps active risk high as well, and does not solve this problem either.

I hope that all investors who do not have an active risk constraint and are therefore not under that pressure make independent and rational allocation decisions regardless of global equity market index weights. Because who guides this world if 100% of investors are tied to index weights? Probably meme investors and the self-proclaimed investment gurus selling investment courses on social media.

I will continue to seek sense in this occasionally highly irrational world through long-term expected returns.

Although Proprius Partners does not invest in the United States, we too can benefit from this enthusiasm. The massive allocation of capital from Europe to the United States pushes down the valuations of many high-quality European companies disproportionately, which means that increasingly excellent investment opportunities land on the desk of our portfolio management team. Of course, the other side of the coin is that the current market ensures, on our behalf, that easy money does not flow into our funds.

At Proprius Partners, however, we focus on generating returns. That is also why we have, among other things, set maximum sizes for our funds in advance. For this reason, we are interested in filling our funds with rational capital. Hopefully this text has once again prompted some thoughts on where future returns will be found.

“Skate to where the puck is going to be. Not where it has been.”

– Walter Gretzky

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Would you like to receive our latest writings directly in your inbox?

Subscribe to our newsletter. We share our views on investing and current market themes.

Lisää luettavaa