Market Letter IX – Make Europe Great Again

Proprius Partners Uusi Eurooppa Non-UCITS Fund

This time, our market letter differs from previous ones in that we are using the opportunity to launch Proprius Partners’ new fund: Proprius Partners Uusi Eurooppa non-UCITS Fund.

At the core of the fund’s strategy is investing in companies that we consider strategically important for Europe, either because of bottlenecks in the operating environment or because of their broader societal significance. This primarily includes sectors and subsectors such as defence, critical technologies, healthcare and infrastructure. The fund’s key objective is to invest in companies with superior competitive positions. Through this, their societal and economic importance to Europe is further emphasised.

In addition to this strategic perspective, we seek to identify companies that can grow clearly faster than European GDP and whose growth is driven by secular themes that carry through cycles, rather than purely cyclical factors. Alongside growth, we also place strong emphasis on company quality. There are numerous criteria for quality investing, and defining quality is often more art than science. At Proprius Partners, quality generally refers to business characteristics such as high return on equity, predictability and visibility of the business, high margins, strong competitive advantages and similar factors. Proprius Partners’ portfolio manager Olli Viitikko has previously written about our approach to quality investing in his blog.

The fund will be managed by Niko Fagernäs, CEO of the company, and Jonas Koivula, portfolio manager of DACH Value. The fund’s launch date is 5 May 2025.

We will communicate more about the fund in the coming weeks as the subscription window opens. If the topic interests you, please contact us and we will be happy to tell you more.

In this market letter, we aim to shed some light on the background factors that have led us to establish this type of fund. The underlying themes have been on Proprius’ radar for a long time, but in 2025 the situation changed decisively, and we now see the fund’s theme as long-term in nature.

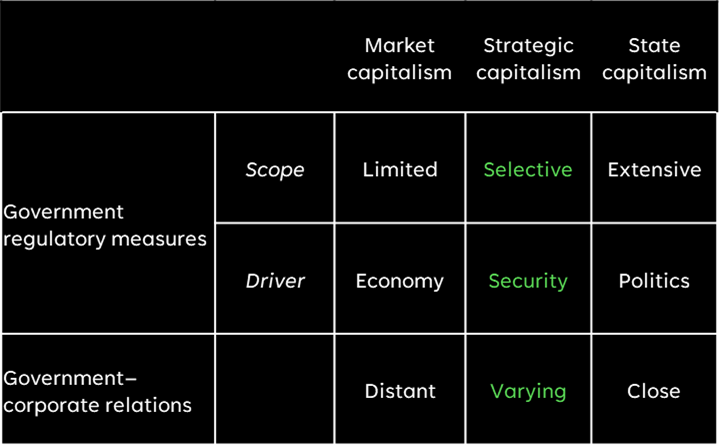

Strategic Capitalism

At Proprius Partners’ second anniversary seminar in January 2025, we heard a presentation on the strategic economy by Mikael Wigell, Research Director at the Finnish Institute of International Affairs. Wigell’s key message was that the world is moving from a traditional economy-driven market economy towards a security-oriented strategic economy.

So what is this strategic economy?

Table 1: Different Forms of Capitalism

Source: Mikael Wigell, Finnish Institute of International Affairs

Put simply, from a Western perspective, strategic capitalism refers to a shift in emphasis: security, rather than the economy, becomes the underlying driver of societal decision-making. In this new framework, the role of the state in business expands, and politics becomes more deeply intertwined with the business environment.

Oren M. Cass, Chief Economist at the conservative think tank Chief Compass, who was also involved in the presidential campaigns of Mitt Romney in 2008 and 2012, comments in his forthcoming book The New Conservatives that US conservatives have historically placed their trust in free markets, but that this is now changing. According to Cass, the starting point is the conservative critique that free markets have led the United States into a situation where, left to themselves, markets are unable to provide answers to the country’s long-term social and security challenges. These include questions such as: can the average American still get by on their wages? Is the United States too dependent on China? Can the United States itself build strategically important components such as semiconductors?

From this perspective, market capitalism does not provide answers to these questions. As a result, there is a growing need to influence how markets function — an idea that is entirely toxic to traditional conservatives. Coincidentally, this new thinking has created Donald Trump’s career as president and explains his slogan “Make America Great Again”.

The US example is important because this shift towards strategic capitalism has gained significant momentum mainly from the United States. In 2018, the United States launched a trade war aimed at preventing China’s influence from expanding beyond where it already was and at restoring the US balance of power. Even then, markets were widely discussing themes such as onshoring — bringing production capabilities back home.

One element of the strategic economy is precisely the use of economic weapons against adversaries. At the same time, security considerations merge with economic policy, while the norms, standards and rules of the global economy and globalisation weaken. This leads to situations where economies are secured through political means, such as the screening of foreign investments, export controls, measures to protect critical infrastructure, and the localisation of data and the digital platform economy. In Wigell’s words, this ultimately leads to the “Balkanisation” of the economy — the fragmentation of economic networks into smaller ecosystems.

One characteristic of the strategic economy is the control of so-called strategic flows. These refer to capital, data, goods, resources, people and services. They no longer move freely from one political area to another, but are subject to tighter control.

Where traditional market capitalism was driven by exports and private capital, strategic capitalism is driven by import substitution, domestic demand and state capital.

The Corporate World as a Battleground

For companies, the situation is complex. In discussions with numerous people over the past few years, we have raised the role of the US Magnificent Seven companies — Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla — and their market positions. In reality, many of these companies have become so-called super-monopolies, meaning they are almost global monopolies rather than traditional national monopolies.

Normally, we would expect more intervention from competition authorities and, on the political side, antitrust pressure to break up these “super-monopolies”. However, viewed through the lens of strategic capitalism, nothing should be done to these companies. On the contrary, from a political perspective, they should be supported even more. Countries need their national champion companies, which can be politicised into economic weapons. A simple example of this is the current US administration’s criticism of European regulation aimed at large US companies. The change is fairly radical: states are stepping onto the corporate playing field and beginning to play a major geopolitical game with companies as their pieces.

From our perspective, this means that different alliances and states will once again start rethinking their approach to global trade policy, their own economic policy weaknesses and dependencies, and through political actions draw companies into this same mix. The logical continuation of this idea is that the corporate landscape will give rise to companies whose role in strategic capitalism is greater than it was in traditional market capitalism.

Viewed from another angle, this means that in order to safeguard their own economic and societal position, states will protect their national champion companies through political means and even support them through various regulatory and financial incentives. This leads to the idea that the growth driver in strategic capitalism is state capital — and that this capital is interested in controlling strategic flows.

What Goes Around Comes Around

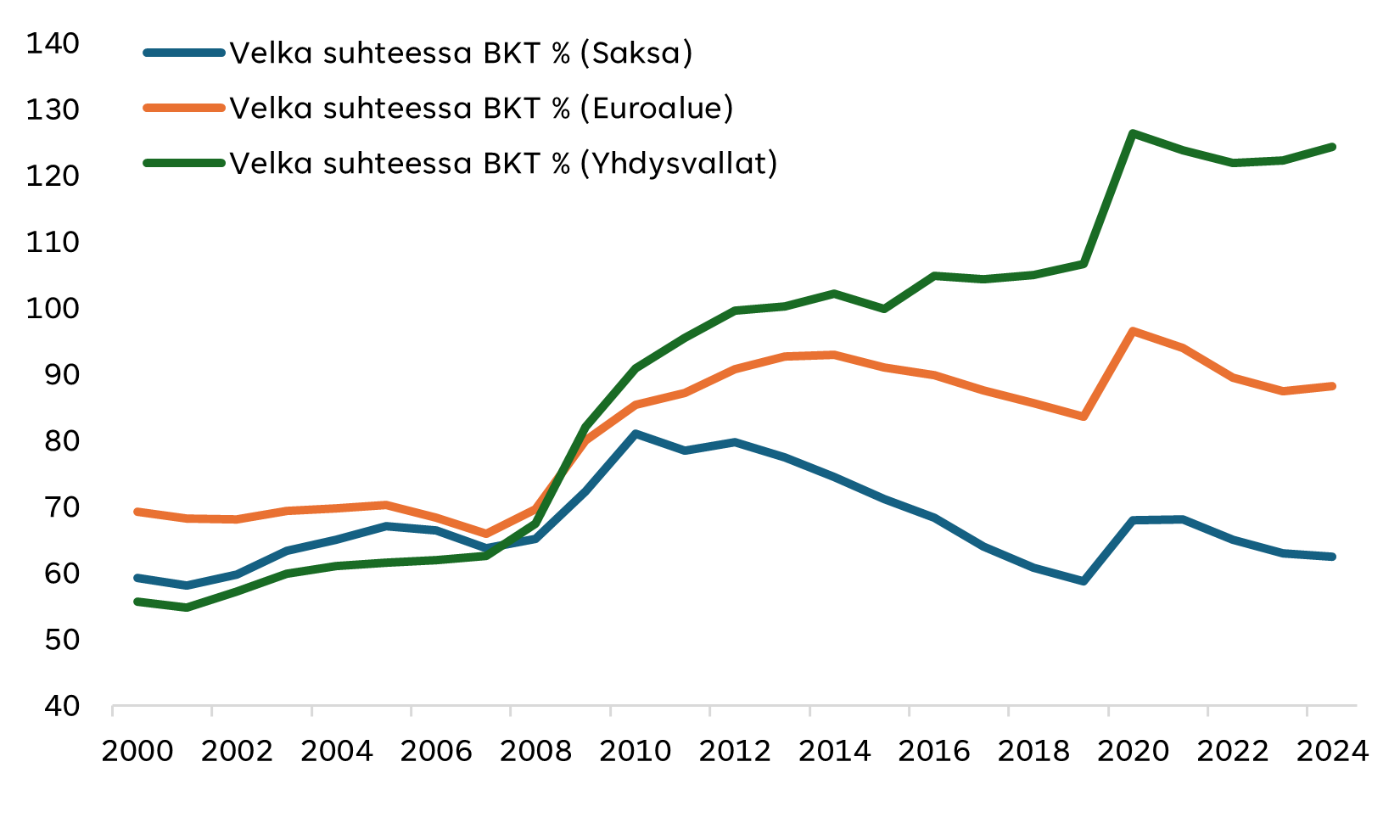

The first steps towards strategic capitalism have already been taken in Europe. They have been directed towards the defence industry. In addition, Germany is investing in infrastructure and domestic investment after these were left completely behind in the 2000s.

Figure 1: Debt-to-GDP development in the United States vs. Germany vs. the euro area

Source: Bloomberg.

In the 2000s, the United States has poured around USD 30 trillion into the economy through monetary and fiscal policy. Over the same period, the market capitalisation of the US equity market has, coincidentally, increased by around USD 30 trillion. It is difficult to establish such a direct cause-and-effect relationship from all the money that has been injected into the system, but the support provided to the economy by the US government and central bank has nevertheless been undeniable.

In the United States, support has often been much more direct to companies and, during COVID, directly to consumers, whereas in Europe support has come indirectly through various mechanisms. In recent years, the United States has introduced new fiscal packages that directly target sectors such as semiconductors, through the CHIPS Act. In other words, the United States has also moved from broader packages towards measures targeted at strategically important industries. The latest major project is Trump’s Stargate project, which aims to pour USD 500 billion into the development of artificial intelligence in cooperation with private actors.

Europe has made very little use of this joint dance between monetary and fiscal policy in the 2000s. COVID was the first example in the 2000s when state purse strings were opened significantly to support the economy, because there was no other choice. In Europe, the general mindset has been one of fiscal responsibility, underpinned by both cultural influences and agreements such as the Maastricht Treaty. The euro area’s monetary rules have so far been clear. We wrote about the German economy last October, so we will not repeat here the dynamics related to Germany, the worst example of fiscal conservatism.

As an economic area, Europe has had a slight structural flaw. We are often compared with the United States, which is a federal state. The US federal government is led by one person whose power has proven to be broad and strong, and historically the federal states have ultimately been united under a single mission. This is not the case for Europe or the euro area. We are not a federal state, even though that sandbox game has been played for some time from the perspective of the European Union.

This lack of unity is a major problem for the European Union. Decision-making stumbles because there are a vast number of conflicts of interest, and we do not feel a genuine cultural bond between countries. In defence terms, this is obviously a question of proximity: the closer countries are to each other, the more they help one another. From the perspective of one’s own security, that response is logical. However, we would argue that cultural distance also matters.

Another European problem, which we often refer to in discussions, is social philosophy. Europe does not share the same social philosophy as the United States. This is clearly visible in economic decision-making and in ideas about how society should be built. Put simply, the entire US society has been built on risk-taking, starting from the country’s founders and founding principles. Europe, by contrast, has been built more around preservation through long-standing monarchies.

The cooperation between the United States and Europe has emerged from compromises between these two social philosophies, united by freedom and democracy — Western values. The United States became the aggressive big brother that ventures out, defends and drives things forward. Europe concluded that big brother would take care of the difficult matters and focused on the welfare of its own citizens at the expense of defence. Big brother was rewarded with good commercial cooperation, investments and European purchasing power.

Now the family has started arguing, as big brother’s hands are so full that Europe, too, should contribute something to this increasingly bipolar world. Europe has been awakened as if someone had dropped ice cubes down its T-shirt.

“Look, let’s be honest, the European Union was formed in order to screw the United States. That’s the purpose of it, and they’ve done a good job of it. But now I’m president.”

– Donald Trump, 26 February 2025

Make Europe Great Again

“The world has changed more in one year than in the previous 30 years combined.”

– Alexander Stubb, 1 March 2025

Europe has woken from its long slumber. It can no longer blindly rely on great-power politics, but must build its own capabilities in both defence and the economy. Security policy is becoming intertwined with economic policy. The interplay between monetary and fiscal policy long used by the United States is now also arriving in Europe, where states are taking a larger role in steering the economy.

During this year, we have already seen announcements of significant additional investments in European defence. Some countries more than others, but the general direction is towards a significant ramp-up of defence capabilities over the next five years. Among EU countries, Germany in particular is setting an example on the fiscal side by investing in its own infrastructure — partly, of course, because Germany has the money to do so.

We believe that capital flows will no longer move to the United States or China in the same way as before, but will instead begin to flow towards domestic markets and Europe. In this case, the impact on the European economy should, in principle, be positive. The recent trade war also shows signs that the United States may ultimately be the loser if it is left alone while others develop trade relationships with one another. Suddenly, Europe looks like the most reliable trading partner.

These new trends will probably also lead to a reassessment of regulation. Europe can no longer prioritise regulating its own companies; it must maximise the competitiveness of its companies for reasons of resilience and security. Deregulation will take a long time, but we have already begun to see the first waves.

Time will tell what role the European Union itself will play in all this. It will face a new test as defence policy is increasingly conducted bilaterally rather than collectively. The first steps in this direction were already seen when France discussed its nuclear umbrella mainly with Germany, before later deciding to expand the discussion to include other European countries as well.

It is possible that, gradually, countries will want to free their own security arrangements from European Union decision-making, where a collection of Putin-friendly countries can throw sand in the gears, and move instead towards bilateral discussions and discussions between different alliances. In this respect, we also believe that it is time to build a tighter Nordic defence and economic alliance on top of existing alliances.

Europe now has its moment to act and shake off the problems that have long eroded its competitiveness. The biggest factor is politics. In the midst of a political crisis, the will now exists. It must be used.

Final Words

When one studies the European corporate landscape more broadly, one finds a huge number of truly fantastic businesses. I still remember comparing the contents of the US S&P 500 Index with the European STOXX 600 Index in 2017 and concluding that there was not much attractive growth to be found in Europe.

Fast forward to 2025, and it must be said that the STOXX 600 Index is no longer the same in terms of content as it was in 2017. When you scratch beneath the surface of the STOXX 600 Index — and also look outside it — you can find companies that are highly significant both at the European and global level, with strong market positions in their respective industries.

Europe has exceptionally high-quality and strategically important companies specifically in healthcare, technology, infrastructure and defence. In all these sectors, there are companies whose role in Europe, and partly also globally, is extremely important, and whose significance for European society is already becoming more pronounced and will continue to do so in the future.

With the new fund, we aim to identify, amid all the confusion, precisely those companies that have an excellent competitive position, are capable of growing, and whose strategic importance to Europe will be significant in this changing world.

Make Europe Great Again!

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Would you like to receive our latest writings directly in your inbox?

Subscribe to our newsletter. We share our views on investing and current market themes.

Lisää luettavaa