Market Letter VIII – Monkeys Throwing Darts, Vol. 2

“I’ll tell you one thing, it’s a cruel, cruel world.“

– Danny Devito

One of my favourite pieces on active portfolio management is Alpha Architect’s 2016 article, “Even God Would Get Fired as an Active Investor.” For the article, they created a study asking what would have happened if, with perfect forecasting ability, one had always selected the best-performing US stocks over the following five years during the period 1927–2016.

The best portfolio would have achieved an annual return of 29.37%, compared with 9.87% for the S&P 500 Index. In other words, perfect stock selection would have generated an astonishing 14.1% annual outperformance for roughly 90 years. The annualised volatility of this portfolio would have been slightly higher, at 22.41% versus 18.96% for the S&P 500. Despite perfect stock selection, the portfolio’s maximum drawdown during the period was -76%, and at worst, it took 1,400 days — almost four years — to climb back to the previous peak.

Alpha Architect also created a hedge fund version, which in the same way perfectly selected the best-performing stocks while also shorting the worst-performing ones. The long-term results were, of course, outrageously good, but even with perfect forecasting, the long/short strategy experienced numerous periods of relative underperformance, at times losing to its index by more than 50%.

So, in practice, whatever one had done, there would always have been periods when things developed so badly — either in absolute or relative terms — that one would have been fired.

Regardless of the chosen strategy, equity markets will therefore hit you in the face from time to time, and sometimes quite badly. The longer the horizon, the more chaos there will be along the way. At times, you will lose to your benchmark completely, 100–0, for a while — until the situation turns. Whether your benchmark is the S&P 500 or your neighbour’s stock portfolio, the long-term outcome improves significantly if you are able to sit through the chaos.

Patience, however, is rare. On average, investors fail to tune out the dissenting voices and other noise that the market constantly pushes at them. Earplugs help, as does accidentally losing your online banking credentials somewhere. But for those who actively follow the equity market, whether as a hobby or professionally, the situation is constantly present.

Figure 1: How to Make Money in the Stock Market

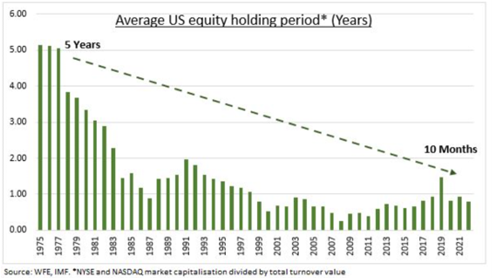

Figure 2: Development of the Average Holding Period for Stocks in the United States

Source: WFE, IMF, NYSE & NASDAQ

The Myth of Market Efficiency

“If I subscribed to the efficient market theory I would still be delivering papers”

– Warren Buffett

Market inefficiency is often used to justify taking views in equity investing. In hindsight, however, conviction investing is often driven more by overconfidence than by the market actually being wrong. Because the market is often not wrong. Despite this, a stock picker must believe, at least to some extent, that the market does make mistakes from time to time.

During my own career, the efficient market hypothesis has been beautifully embodied in the value investor’s favourite enemy: value traps. Value traps are the classic example of how investors overestimate their own ability and underestimate the intelligence of the market. I wrote about this topic, among other things, in “A Headache as Compensation,” published in May 2024.

“If markets were gigantically, obviously and often inefficient, people would come in and take advantage of all these inefficiencies in a far easier manner than seems to happen in real life”

– Cliff Asness, AQR

Practical experience also shows that stocks sometimes exhibit fairly radical distortions. There are countless stories of these market distortions where it is quite easy to see what will happen, but not when it will happen. There are also countless cases where seemingly clear arbitrage opportunities simply did not play out as they should have, and investors ultimately burned their fingers. This is often a case of so-called limits to arbitrage. It means that, due to a combination of many factors, obvious arbitrage situations do not correct themselves as expected.

“The market can remain irrational longer than you can remain solvent.”

– John Maynard Keynes

Benefiting from these inefficiencies is precisely one of the most important sources of added value for an active equity investor. Markets are almost constantly wrong in some way, and sometimes much more wrong. As noted, however, these distorted situations do not necessarily correct themselves magically — and even if they do, the investor has probably thrown in the towel long before.

“Offsetting actions by informed investors do not typically suffice to cause the price effects of erroneous beliefs to disappear with the passage of time”

– Fama and French 2007.

Incorrect views become more pronounced the more money is poured behind them. Taking the other side of the trade is therefore often a fool’s errand. That is why many eventually give up and become momentum investors. All other styles are psychologically too difficult. Hedge funds know this better than anyone, as quite a few of them have collapsed over the years around this very theme. Ironically, hedge funds’ correlation with the S&P 500 tends to rise at regular intervals.

Anomalies — The Lifeblood of Active Equity Investors

” We search through historical data looking for anomalous patterns that we would not expect to occur at random.”

– Jim Simons

In our view, the failures of market efficiency are what active equity portfolio management lives on. Market participants like Proprius have historically relied for a long time on the value and small-cap anomalies. By anomalies, we mean investment strategies that appear to systematically generate excess returns relative to risk, returns that traditional financial theory models cannot explain.

These two anomalies have long rested on a fairly solid foundation, but their effectiveness has varied significantly depending on factors such as geographic focus and others. Value investing, in turn, is a very popular style, but since the financial crisis it has been unusually weak as an investment style. Both anomalies have stumbled very badly recently. As I said, there are no silver bullets in investing.

Value investing is, however, strongly supported by risk thinking. Most often, value investing is characterised by low expectations and, consequently, low valuation multiples. It is often easier for value companies to meet market expectations than for more expensive companies. One often hears that there is “ground beneath the feet” in valuation multiples. Of course, having ground beneath your feet does not help much in determining how high you can jump. For that, you need your own leg muscles.

Figure 3: The Pessimist Is Not Disappointed

Source: Dechow & Sloan, 1997

In their 1997 study, Dechow and Sloan argued that value stocks outperform because the market relies too much on analysts, who are overly optimistic in their earnings forecasts and also fail to anticipate mean reversion in company fundamentals. This mean reversion has been seen as a kind of natural law that ultimately always applies.

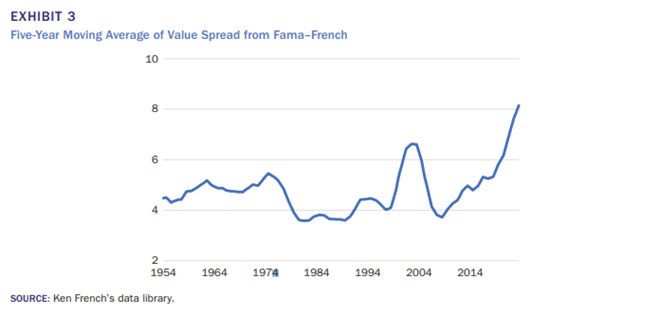

Figure 4: Five-Year Moving Average of Valuation Spreads Between High and Low Price-to-Book Companies

Source: Cliff Asness, AQR

The gap between value and growth companies has kept widening. The figure uses the price-to-book metric, which naturally attracts plenty of criticism over whether it is still the right measure today. In reality, this hardly matters. One reaches largely the same conclusion using a long list of different valuation metrics and combinations of them. Nor does the criticism that value today lies in intangible assets materially affect this calculation. In addition, if small caps are added to the calculation, almost nothing changes.

Mean reversion has not happened. Quite the opposite, in fact. The strongest explanation for this phenomenon so far is probably that the world has drifted into a winner-takes-all type of economic system, meaning that the corporate landscape has gradually become fully monopolised. This effect has created an extraordinary amount of wealth for index investors, who can simply sit on top of this trend with virtually no constraints. For active equity funds, this is more difficult. Regulation restricts fund concentration, but it does not restrict indices. In the era of such super-monopolies, such as the famous Magnificent 7 in the United States, the S&P 500 Index dominates almost all active portfolio managers, regardless of where they invest. As the well-known saying goes, in the end everyone’s benchmark is the S&P 500.

Winner-takes-all also applies to allocations and the movement of money around the world. In the 2000s, the weakness of the value style lasted such a short time that asset allocators around the world did not really have time to change their investment beliefs. What matters most is not how extreme these valuation spreads become, but how long the trend and the levels persist. Now value investors have endured a painfully long journey, which has effectively killed the entire investment style as the backstop has failed.

The same has likely happened to small-cap investing, where the decline from the highs of the COVID crisis has been so direct and brutal that there are not many survivors left.

So the good old anomalies are, for the time being, broken. What has replaced them?

The Herd Follows Price

“Buy stocks that go up; if they don’t go up, don’t buy them”

– Will Rogers

The momentum phenomenon has consumed almost all the oxygen. In the era of the impatient investor, it is an excellent medicine. The momentum anomaly is by no means a new phenomenon. It is a market phenomenon more than 200 years old and is often called the grandfather of market anomalies. There are many kinds of momentum strategies, but in this text I am referring specifically to the original and most widely used momentum strategy: price momentum.

Momentum is an even simpler strategy than value or small-cap investing. It involves taking the stocks that have performed best over either the past three or six months in a selected geographic region and buying them. The portfolio is then adjusted every three or six months, always buying the stocks whose share prices have performed best. No fundamental analysis is performed; only price is bought. This way, one only buys rising stocks — at least from the rear-view mirror.

This strategy is one of the most astonishing examples of market inefficiency. The idea that share price and its development alone could support outperformance represents the breakdown of the weakest form of market efficiency. Yet in today’s world, this stock market anomaly has relatively good arguments behind it:

- A winner-takes-all environment feeds directly into momentum’s hands. The same companies capture market share and generate extraordinary margins. Their share prices perform well and continuously end up in momentum strategies.

- The size and net purchases of passive investment solutions interact with the momentum anomaly. Passive investment products buy market capitalisation. The bigger the company, the more they buy. At the same time, the more they buy, the more upward pressure there is on stocks due to demand. The more the stocks rise, the more momentum buys them. Round and round it goes.

- The change in market participant behaviour caused by technology has made investors more impatient, effectively driving them to buy price rather than value. This too supports the positions of momentum-style strategies.

Despite these favourable starting points, momentum is often said to work until it suddenly does not work at all. Momentum performs best when certain market segments continue to do well for a long time, but it suffers significantly if there are many style shifts in the market or if general market sentiment turns sour.

Momentum is therefore a beautiful solution for this chaotic investment environment, bringing psychological clarity to the strategy. Just buy rising stocks and you do not need to think much more than that.

Figure 5: A Momentum Investor Throws the Value Investor’s Bible in the Bin

The Uncomfortable Truth

“Uncertainty is an uncomfortable position. But certainty is an absurd one.”

– Voltaire

If generating returns is as simple as just following returns forever, what on earth is the point of analysing companies beyond their share prices and price development? Is exploiting market inefficiencies even sensible if the inefficiencies do not disappear, or if it takes forever for them to disappear? Why did I not put all my money into Trump’s crypto coin?

Long-term equity investing is psychologically difficult. At times, it can even be impossible for the human mind. Long-term thinking is easy in theory, but almost impossible in practice. Do we fight until the final bell, or where does long-term commitment actually die?

The death of long-term commitment most often comes either from interpreting an investment as a mistaken investment or from making an investment mistake. A mistaken investment is often justified by a wrong view or by not having done enough research. Unfortunately, the distinction between a mistaken investment and an investment mistake often becomes blurred in these cases.

By an investment mistake, we mean an individual investment decision driven more by bad luck than by the investor having made a systematic process error. Most often, investment mistakes are made when risk tolerance and discipline begin to fail. Classic investment mistakes include trading stocks back and forth, panic-selling at the bottom, or buying at the top because of FOMO. Mistaken investments happen to everyone and are an essential part of long-term investing, but investment mistakes should be avoided to the very end, because they lead to lost returns.

Figure 6: The Cost of Investor Overactivity

Source: Morgan Stanley

It brings to mind going to the gym or doing sports. Many people do it with discipline for a while, but how many do it consistently for 10 or 20 years without interruption? Quite often, Magnificent 7 companies eventually slip into portfolio managers’ portfolios because there is no point fighting them anymore — or the job disappears from under you. Of course, views can be changed, and often they should be changed if the facts change. But risk can never be hidden from. Risk always finds the investor eventually in the equity market. There are no silver bullets in equity investing, and there never will be — except diversification, of course.

“Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom.”

– David Swensen

The truth, however, is that if one wants to achieve so-called better returns than the market in general, one must do something uncomfortable. Warm, cosy and comfortable investing rarely produces the highest returns. In this context, David Swensen’s quote has merit. Following this logic, I would like to tip my hat to crypto investors for the success they have achieved so far, regardless of what I personally think.

AQR’s Cliff Asness states in his piece “The Less-Efficient Market Hypothesis” that investing has always been a challenge combining two things: 1) distinguishing the correct hypothesis from the wrong one, and 2) sticking with the chosen hypothesis.

From Proprius’ perspective, distinguishing the correct hypothesis from the wrong one is not the difficult part. The most difficult part is sticking with the hypothesis.

We will continue to focus on value and small-cap investing, even though it can at times be painful and require patience. We believe that a long time horizon and a disciplined strategy ultimately produce the best results. Markets constantly test patience, and short-term pressures may tempt investors into quick decisions. We remain faithful to our principles and investment philosophy, even if the areas we have chosen may currently look foolish to some.

Following Swensen’s thinking, we believe that precisely those uncomfortable areas that investors avoid are the ones that eventually produce excellent returns, as long as they are given time.

Wishing you a good start to the year,

The Monkeys Throwing Darts

Proprius Partners Oy (hereinafter Proprius or the company) has prepared this material, which is not part of the company’s official product documentation. The information presented may contain Proprius’s general information and views at the time of publication, which may be changed without prior notice, and which are based on Proprius’s best estimates and opinions derived from information compiled from public sources it considers reliable. The aim is to provide information that is as accurate and correct as possible, but Proprius or its employees cannot guarantee the accuracy or completeness of the information, estimates, or opinions presented, nor are they responsible for the accuracy of information obtained from third parties. The information presented in the material may have changed or may change after the material was prepared.

The presentation or the information contained therein does not constitute investment, tax, accounting, or legal advice, an invitation to trade or take other investment actions or to refrain from doing so, and cannot under any circumstances be considered an offer to sell or buy a financial instrument.

The return expectations presented are indicative estimates only and do not constitute promises of future returns or interest. The return an investor receives from the product is determined by market developments. Future market developments are uncertain and cannot be accurately predicted. Historical returns are not a guarantee of future performance. The client may lose part or all of the invested capital. The information presented is not based on impartial investment research or analysis of the financial instrument’s issuer or the underlying assets of the financial instrument.

Before making any investment decision, the client should always review the official documents published by Proprius at www.proprius.fi/en/documentation or at Proprius’s office. The client is always solely responsible for the financial consequences of their investment decisions and orders. Proprius is not liable for any direct, indirect, or consequential damages or losses that may result from theuse of the information presented in this material. Proprius is supervised by the Finnish Financial Supervisory Authority (Finanssivalvonta). This material is protected by Proprius’s intellectual property rights and may not be reproduced, published, or distributed in any way without prior written permission from Proprius. All rights reserved.

Lisää luettavaa